patrick.net

An Antidote to Corporate Media

1,202,333 comments by 14,267 users - Rin, WookieMan online now

« First « Previous Comments 93 - 132 of 219 Next » Last » Search these comments

You always rent unless you live under a bridge. The question is just what you are renting.

1) house

2) money from a bank to pay off house

3) your own investment money to pay off a house

People think owning a home means you are free and clear. Owning a home means less mobility, more maintenance, loss investment growth, etc. A house is not an investment. It is a functional asset that keeps our body protected from the outside elements. You own it just as much as you own the water that flows in your toilet. We are renting everything, don't be fooled.

Ding Ding Ding. We have a winner! Vanna, tell him what he's won...

Vanna: you win 24/7 access to Benjamin Bernanke. Call him anytime you need some money. Fuck up your finances? No problem. Uncle Ben is there to bail you out.

APOCALYPSEFUCK is Tony Manero says

Plant potatoes and teach the family hand to hand combat skills.

Actully I did that, HAGANAH!

Who sets prices ? (supply & demand

Not for housing unfortunately

Especially for housing.

BUYERS MAKE VALUE ! No one else.

Fat people are still eating too much and home buyers are still paying too much. LOTS of denial out there.

If you had the most magnificent palace in all de land. But there were NO buyers. What is de value ? That's right, NADA F-ckin thing.

If you are selling a quanset hut , and there are 20 people in line wanting to buy and 19 people are offering $500k and the 20th guy offers you $600K. What is the value ?

Gubmint is trying to buffalo the masses because that is what we want them to do. We want gubmint to prove to us that "all is well". They will generate false hope only to be reelected or til the money runs out.

Inflation is coiled like a snake and about to spring forth, crushing everything gubmint has been offering. We will look back and see tarp, & hemp & harp in their true colors. B.S.BROWN.

What we need to do is boycott real estate for one year, That should finish off the banks and send most realtors back to school.

Especially for housing.

BUYERS MAKE VALUE ! No one else.

Think about it like this. If people were forced to use real money (not the future money they hope to make) to pay for a house, then you have a supply/demand market. When there is a free money train that comes through town and writes note for basically free money that people can use to buy homes, then the market gets distorted.

People are not really weighing the amount their paying against the value in the asset they are getting. Not their fault, they are victims in this ponzi scheme as well. Like every ponzi scheme though, you either run out of friends or run out of money. We have already run out of money, we just are in denial.

You watch this a minute and then predict how this will end. Hint: in a world of hurt for Americans. (of which I am one)

HEY TAZ,

That clock reminds me of a friends advise for watching a train wreck in progress. Wait til it's over and pick up the pieces. I hate that advise. That is like saying "let the drug addict (gubmint) hit bottom" while they are destroying our economy.

People are not really weighing the amount their paying against the value in the asset they are getting. Not their fault, they are victims in this ponzi scheme as well

Do you mean ? Take a bare piece of land add $65 to $100 per square foot for building costs and you have the actual value ? If Bill Gates & Gary Coleman both bid on that property, who ya gonna call ?

Not a ponzi scheme so much as a marketing scheme. DeBeers forces competition & high pricing by distorting supply. OIL is valued according to our addiction. If you can't pay $7 bucks a gallon, step aside till the more affluent makes up the margin. Land developers realized they overbuilt and won't build today.

Our mentality is manipulated by all types of sales people. In real estate,

At the mere suggestion to a sales rep that you would like to buy a home, the FIRST question is "WHAT IS THE MAXIMUM YOU CAN AFFORD TO PAY"? The second question is "how much MORE can be SQUEEZED out of you. Buyers are pussies. They should be telling the sellers what it is worth, NOT the other way around ! BUYERS have fluidity and inventory on their side.

The insane justification for buying homes from the mid 70s till the bubble popped was, "pay anything, it will be worth 20% more next year". There are still buyers anticipating a "RECOVERY". That is just more marketing.... Negotiating tomorrows prices should include yesterdays insanity. Prices will crash till demand (jobs) increase.

Gubmint has spent trillions using the word "RECOVERY". While sacrificing the old (zero interest rates) and the young (your grandchildren will probably not enjoy appreciation or pensions). Mayan cultures performed similar rituals during droughts. They sacrificed the Old & the Young because they could not fight back.

You always rent unless you live under a bridge. The question is just what you are renting.

I can't believe how many smart people perpepuate this nonsense. Renting and owning are different.

Yes, when you own with a mortgage, you owe the bank payments on your loan. The bank, however, doesn't own the home. You do. You have put up the house as collateral on the loan.

Yes, when you own, you have to pay property taxes. The locality doesn't own the property, however. You do.

There are valid reasons to rent, but being afraid of debt slavery shouldn't be one of them.

Two guys I know asked me to lend them money to pay off their mortgages. They heard that interest rates are low. So, they both said to me: "Led me $150K, I would pay you much higher interest than you are making today."

I said "I'll pass. Thank you for your interest in helping me find higher interest on my capital."

Everyone who thought they were "rich" buying a property now see it as an expensive albatross unless they work for the government, are doctor/lawyer, etc.

Your results may vary.

hrhjuliet : I know you've got the info you needed - personally I think you made the right decision - for now.

It's interesting to see someone hash out their thinking and personal situation in a public forum - to see how their thought processes work.

Personally, we are in a somewhat similar situation - we have money saved, are looking for a house, two kids etc. However, I personally would be scared spitless to have money in the markets right now (any markets). They are all a disaster just waiting to happen IMO - things like high frequency trading (HFT), MF Global and the like would make it impossible for me to sleep at night. A 100+ percent gain in 2+ years is NOT healthy functioning marketplace. But it's your money to lose. I sleep very well with all our money in cash, spread in several credit unions in non-money market funds. It's the safest and most liquid thing I can think of - return OF capital versus return ON capital. And you're talking to guy who has done a lot of high risk trading in the past - the kind where you lose 400k in 45 minutes LOL

No more. The stakes right now are too high.

The BA is a very odd place in that, as long as there is some tech presence there prices will always be skewed upwards. For someone like you, with your business you really have very little freedom to live elsewhere.

For my family, we are going the route discussed above - saving our money to buy a house outright in a decent weather area (very very important to me) and going into semi-retirement. That's a big lifestyle change, but I'm not willing to spend 20 to 40 years sitting in a cube, dreaming of being elsewhere.

It's my considered opinion that we as a society have been balanced on the edge of a cliff for years now, just waiting for a push into the abyss economically. Even when that happens, it almost certainly won't be an overnight thing. But when it does happen, those who are going to be hurt the least (and that is the best you can hope for at this point - to minimize the pain) are going to be those who have invested the least (emotionally and financially) in the religious belief called 'faith in the system / status quo'.

IMO Things are going to change (for the worse) in the next 5 to 10 years more than you could ever believe and a person's best efforts right now should be oriented towards mitigating the damage. Buying a house in one of the last true bubble RE markets in the USA is probably not the best way to accomplish that.

I say don't buy yet b/c prices are still dropping. Interest rates are artificially low which is propping up the housing market. It's much better to buy when interest rates are higher and housing prices are lower - esp in CA. If you buy when prices are lower you are locked in to lower property taxes and lower level of indebtedness. Eventually interest rates will revert to historical mean and housing will take another hit. Of course it also depends on your circumstances. 500 sq ft is pretty tight for a family of four. If you don't plan on moving for at least 10 years and can ignore the headlines when the value of your house drops then maybe you should buy. It would be a bummer to buy with a 3% loan and have the value of the property go down 20% when interest rates go up to 6% or higher - it doesn't matter unless you want to sell but still, it's a bummer.

I didn't want to regret not bidding and I didn't want to regret

hrhjuliet saysI'm afraid of regrets, but I'm also afraid of making the wrong choic

but don't want to rush in if this is a bad time.

Not to mention I would be afraid

It sounds like you need to confront then resolve your fear factors first. People who are important in your life are not going to hold you accountable if your decision turned out not to be the Most Excellent Choice. Only time would tell on that one. And if people do hold it against you, then by definition they are not persons who are important to you, even if you think that they are.

Imagine if young Americans on the beaches of Normandy, or the victims on United flight 93, or Caption Sullenbreger were motivated by fear of regret or fear of not timing things perfectly.

It's much better to buy when interest rates are higher and housing prices are lower - esp in CA

Unfortunately, history shows that doesn't happen.

tatupu - what do you think will happen when interest rates inevitably go up to 5 - 6 - 7% or higher? I'll tell you - affordability goes down and so does the price of housing. The artificially low interest rates fueled the bubble and continue keep prices inflated. The best time to buy is when rates are high, prices are low and the market is dead. It's happened more than once in my lifetime (I'm in my early 50s) and I believe it will happen again. There is also the advantage of locking in a low property tax rate, which in CA can last a lifetime.

russell,

If you say so.

But Hipsters and wealthy immigrants will tell you no

It's different this time.

It's different here.

Purchase Price in PARAMOUNT!!!

Interest rate is not that important. I also have experience in previous cycle and market indeed will come to dead zone very soon. Recently we have very low inventory due to the following facts:

1. Houses for sale are mostly represented by short sales and foreclosure with extremely low number of regular sales. Apparently many should be regular sellers hold they breath, thinking we are in the bottom and rebound is just other the corner. That will not happen unfortunately, so seller will have no choice and list house on market to various reasons: kid’s outgrown, new kinds, divorces, job transfers, to name a few.

2. Facebook and other IPO’s is just another propaganda spread by realtors to create fear (yes, our nation is so good with it)

3. Low interest rate create another fear (can go only up!). Didn’t happen in Japan.

4. OMG multiple offers! Look bellow (Santa Clara county), yes we have multiple offers but not above asking price. January statistics: Sale vs. List Price - 99.0%!

Indeed, every cycle is different, but has same stages. If you found great deal – go for it. If not, don’t PANIC. Real Estate does not behave like stock market.

Trends At a Glance Jan 2012 Previous Month Year-over Year

Median Price $485,000 $532,000 (-8.8%) $524,000 (-7.4%)

Average Price $642,128 $716,061 (-10.3%) $649,476 (-1.1%)

No. of Sales 649 899 (-27.8%) 682 (-4.8%)

Pending Properties 1,678 1,528 (+9.8%) 1,329 (+26.3%)

Active 1,466 1,386 (+5.8%) 1,757 (-16.6%)

Sale vs. List Price 99.0% 98.7% (+0.3%) 98.9% (+0.1%)

Days on Market 66 63 (+4.7%) 67 (-1.0%)

tatupu - what do you think will happen when interest rates inevitably go up to 5 - 6 - 7% or higher? I'll tell you - affordability goes down and so does the price of housing. The artificially low interest rates fueled the bubble and continue keep prices inflated. The best time to buy is when rates are high, prices are low and the market is dead. It's happened more than once in my lifetime (I'm in my early 50s) and I believe it will happen again. There is also the advantage of locking in a low property tax rate, which in CA can last a lifetime.

The only problem with that is that it isn't supported by the facts. Look at historical housing data - house prices very often continue to rise even as interest rates go up. You are waiting for something that may very well never happen.

tatupu - what do you think will happen when interest rates inevitably go up to 5 - 6 - 7% or higher? I'll tell you - affordability goes down and so does the price of housing. The artificially low interest rates fueled the bubble and continue keep prices inflated. The best time to buy is when rates are high, prices are low and the market is dead. It's happened more than once in my lifetime (I'm in my early 50s) and I believe it will happen again. There is also the advantage of locking in a low property tax rate, which in CA can last a lifetime.

The only problem with that is that it isn't supported by the facts. Look at historical housing data - house prices very often continue to rise even as interest rates go up. You are waiting for something that may very well never happen.

Please reference the data you are referring to here. I would love to be enlightened here.

It's much better to buy when interest rates are higher and housing prices are lower - esp in CA

Unfortunately, history shows that doesn't happen.

Can you reference the history of the relationship between real house prices and interest rates? It would be helpful.

Yes, when you own with a mortgage, you owe the bank payments on your loan. The bank, however, doesn't own the home. You do. You have put up the house as collateral on the loan.

Please tell the jury who holds the title to the home during this process. "uh uh uh, The banks holds the title but but but...."

So, if the current person living in the house decided to not make the agreed upon payments then does the bank have any ownership rights to the house? "Um yah, but but you are being misleading here, house prices always rise, history shows that, so there is no worry about a mortgage holder missing payments".

Uh um, please answer the question. It is a Yes or No. "well um uh I guess if you had to say the answer and it really". Please please just answer the question for the jury. "I guess it would be yes then".

So, the person living in the house really only has an obligation to use the house while the bank is owning the title. If that fore mentioned person completes the required payments on time like outlined in the mortgage agreement then they will receive title and be the new owners. Would that be a fair assessment? "Um uh um uh, Look a Puppy!" as tatupu runs out of the court room never to be seen as a real estate expert again.

Executive summary: Bank owns the house. You rent money or a house. If you think otherwise then you don't understand the real estate ponzi scheme disease that is killing this country and you must really be confused each year we drop further and further into the abyss. Real estate is dead. Deal with it.

I say don't buy yet b/c prices are still dropping. Interest rates are artificially low which is propping up the housing market. It's much better to buy when interest rates are higher and housing prices are lower - esp in CA. If you buy when prices are lower you are locked in to lower property taxes and lower level of indebtedness. Eventually interest rates will revert to historical mean and housing will take another hit. Of course it also depends on your circumstances. 500 sq ft is pretty tight for a family of four. If you don't plan on moving for at least 10 years and can ignore the headlines when the value of your house drops then maybe you should buy. It would be a bummer to buy with a 3% loan and have the value of the property go down 20% when interest rates go up to 6% or higher - it doesn't matter unless you want to sell but still, it's a bummer.

Finally some forward thinking on this site that actually makes sense. I don't understand why everyone can't see this logic. What is said here I also believe to my core. I wish it wasn't, but the greed and manipulation of the last 10 years is on the road to recovery. On that road will be a lot of hurt people. Some good, some still greedy. Such for the good, so I hope others hear this stuff and get out of dodge to avoid the crap that will hit the fan. 685K debt per family! Come on, how the hell are we going to dig out of that hole? We are not.

The only problem with that is that it isn't supported by the facts. Look at historical housing data - house prices very often continue to rise even as interest rates go up. You are waiting for something that may very well never happen.

Does the par value of a bond fall when interest rates rise? Yes. ALL the time, EVERY time.

Stop lying to the public.

Realtors Are Liars.

That's just another daft post from you. A house is not a bond, and it's price isn't as directly dependent on mortgage rates as people seem to think. I mean for crying out loud, interest rates were going up in 2006. What happened to house prices? That's one, very recent, example that shows other factors play an important role in determining prices. That's why it's wishful thinking for people to just say "I'm waiting for interest rates to rise because house prices will fall." Well no, not necessarily. What about correlations between house prices and income and population growth. If the interest rate was the be all and end all, then house prices/sales would be doing very well right now.

And here you go:

So, if the current person living in the house decided to not make the agreed upon payments then does the bank have any ownership rights to the house?

Sure-it's a condition of the loan agreement. So what?

So, the person living in the house really only has an obligation to use the house while the bank is owning the title. If that fore mentioned person completes the required payments on time like outlined in the mortgage agreement then they will receive title and be the new owners. Would that be a fair assessment?

No--they have repaid their loan agreement. And the collateral is returned to them.

Executive summary: Bank owns the house. You rent money or a house. If you think otherwise then you don't understand the real estate ponzi scheme disease that is killing this country and you must really be confused each year we drop further and further into the abyss. Real estate is dead. Deal with it.

Wrong again. I'm sorry you have such a poor understanding of property law. Read up and then you can try again.

tatupu - what do you think will happen when interest rates inevitably go up to 5 - 6 - 7% or higher?

I think the economy will be recovered, inflation will be higher and incomes will be growing. And house prices will be rising as well. Historically, that's what has happened.

Can you reference the history of the relationship between real house prices and interest rates? It would be helpful.

#1--we're talking about nominal home prices, not real.

#2--Historically, there is no correlation between nominal home prices and interest rates. And it's easy to explain why. Home prices are most dependent on income and incomes rise during good times. And guess what--interest rates are higher during good times.

Yeah, houses are exactly like bonds, except where they aren't. And we aren't talking about inflation - you and others have been saying that higher interest rates = lower prices. The graph shows that that is a massive over simplification. If all things held equal, then you could argue your case about interest rates, but they don't.

And I was under the impression that house prices were relatively flat during much of 2006 whilst interest rates were rising. The subsequent collapse in house prices wasn't driven by that relatively small rise, or are you seriously trying to argue that they were?

Wrong again. I'm sorry you have such a poor understanding of property law. Read up and then you can try again.

Hence why we are in such a mess. If I sold a piece of property to someone that was unable to make full payment, I consider that property (or collateral as you call it) mine, until full payment has been paid. If you damage, burn down, misuse, etc. my property then I am the one losing. Hence, why the mortgage issuer requires you to get the proper insurance. Try to get a mortgage and tell them that you don't require insurance on your home (you know, the one you own). You will quickly realize who has the vested interest, and who the rightful owner is.

You are obviously stuck in a rut and not until the ponzi scheme collapses completely will you see things properly. Good luck the next 5 years, you will need it.

Can you reference the history of the relationship between real house prices and interest rates? It would be helpful.

#1--we're talking about nominal home prices, not real.

#2--Historically, there is no correlation between nominal home prices and interest rates. And it's easy to explain why. Home prices are most dependent on income and incomes rise during good times. And guess what--interest rates are higher during good times.

Perfect, thanks for the data and graph. Wow, I see it now. ;)

And here you go:

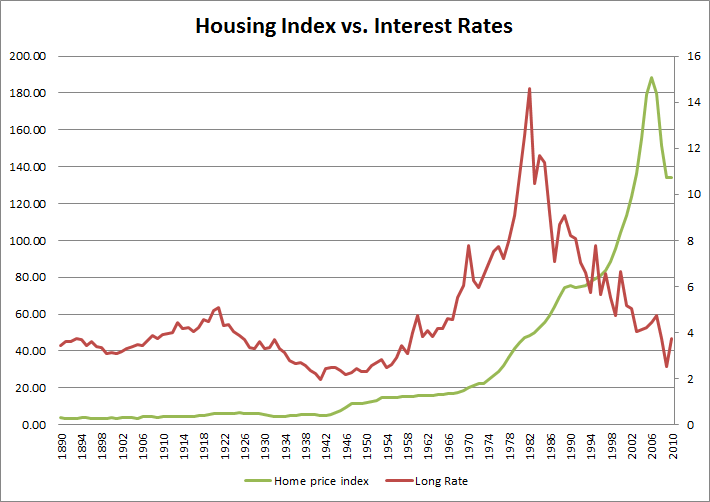

From you own graph, the people that benefited the most from housing were the ones who bought in 1984 when interest rates were the highest and the housing index was just start to rise. Then as the rates started to collapse in order to support and even futher increase in the house index (adding greed by many to the equation) the owners would just refi. Now they have the benefit of a low payment and an increasing house price. Perfect! Fast forward to today and we have a completely different story with nothing pointing in a positive direction for the buyer. The benefit is gone, and will only return when interest rates rise again. You need to buy when they are high and refi as they are going down. That is how money is made in housing, not the other way around.

You can select any small periods of time and argue what you like, but the general trends show that there's a lot more going on than simply stating that higher interest rates will mean lower prices. And housing started rising from a low in '81, didn't it? And yes, interest rates played a major role in the 80s, but then again they did reach up to 16% or so, and as you follow the real house prices and interest rates, there are periods where yes the correlation holds and when it doesn't (interest rates rose 83-84 as did house prices for example, and then there was a long period from 86 or so to 91 where rates were flat and house prices declined substantially).

Anyway, my point isn't that interest rates don't have a role in house prices as they obviously do, but that it is by no means the only factor in determining what house prices will be at any given time.

Don't waste your money buying something you will not be happy with. These insanely high prices can't and wont' sustain themselves forever.

I wouldn't compromise if I were you, it's a lot of money to buy something you won't love and will probably grow to hate.

It's a price repeat of DotCom. During DotCom people were buying very expensive houses because those involved were making money hand over fist. And as soon as that ended, all those insane IPO's came to the end it crashed. If I were you, I'd expect the same repeat. It's no different today.

One of my old clients used to make a lot of money during DotCom, due to IPO's and overvalued stocks. When that ended, they ended up foreclosing, and prices dropped a lot too. Amount of money went away, and prices went down.

Perfect, thanks for the data and graph. Wow, I see it now. ;)

since another poster pasted it already, I didn't see the need to duplicate his work.

Did you not see it?

I rest my case your honor.

Thanks for proving that the only way you can make your case is by deception.

Perfect, thanks for the data and graph. Wow, I see it now. ;)

since another poster pasted it already, I didn't see the need to duplicate his work.

Did you not see it?

And it was debunked already. It doesn't show what you both are saying. Not even close. The best time to buy real estate is when interest rates are at the peak or heading towards the peak, not the other way around.

Perfect, thanks for the data and graph. Wow, I see it now. ;)

since another poster pasted it already, I didn't see the need to duplicate his work.

Did you not see it?

Correlation factor is not at all obvious like you say. Here is what I see in the graph.

1902-1920: Int up, Houses flat

1922-1942: Int down, Houses flat to up

1954-1962: Int up, Houses flat

1970-1982: Int up, Houses up

1982-1988: Int down, Houses up

1988-1991: Int down, Houses flat

1991-2006: Int down, Houses up

2006-now : Int down Houses down

The only correlation I see is that when there is a runup in prices like now there will be a correction in prices no matter what happens to the interest rate. The rates are normally adjusted down in an attempt to stop the drop, but at best it keeps prices flat or the drop continues (like now). The correlation that low interest rates are the best time to buy, I just don't see. It actually looks like the worse time to buy to me in terms of future price appreciation potential.

I think both sides are correct here. It is not a good time to buy now because of low interest rates. But as rates start to rise then that might turn out to be the best time to buy. That is normally when prices of housing starts to appreciate the best. Probably because it means we have come out of the woods are things are on fire for the economy to justify the raise in interest rates. Remember, they are raised to cool the economy. So, if we start seeing interest rates rise we all should really cheer.

Anyway, my take on the graph. I'm sure others will see it differently.

RentingForHalfTheCost says

So, if the current person living in the house decided to not make the agreed upon payments then does the bank have any ownership rights to the house?

Sure-it's a condition of the loan agreement. So what?

Lets try again. I'll answer the "so what?" This means the bank owns the property until you satisfy the mortgage. That is why they hold the title. If you are the rightful owner then ask the bank for the title. Shouldn't you own the title if you are the house owner? Damn right you should. I have 4 titles on my properties in my safe and am the owner in a sense. I can still lose the homes to the city if I don't keep up on the property tax payments. So, there is a bit of pseudo ownership going on. I'll take the pseudo over the owning a mortgage any day though. Mortgages are an easy way to put and keep yourself in debt for life. Did you see the bonuses given to bank executives, Freddie and Fanny Mae executives. Guess who is paying for all these bonuses?

I never said that low interest rates were the best time to buy. I said that there wasn't an automatic correlation between high interest rates and low prices, so I'm not quite sure what you think you've debunked. Your own list above doesn't even match what you've been arguing. Trying to predict when the best time to buy is is a pretty futile exercise. There are far too many unknowns for people to truly know what is going to happen. To me, it looks a pretty good time for a lot of Americans to buy a house - prices are pretty low (in terms of multiples of salary) in many parts of the country and interest rates are at historically low levels. Now that doesn't mean everywhere makes good sense. This place seems heavily focused on the BA and prices seem quite a bit more out of whack there compared to many places. Fine, wait it out if that's what you want to do, but then people shouldn't generalize it out to the rest of the US by pretending the situation is the same everywhere. It clearly isn't.

I never said that low interest rates were the best time to buy. I said that there wasn't an automatic correlation between high interest rates and low prices, so I'm not quite sure what you think you've debunked.

I was caught up in two conversation, so sorry it wasn't perfectly clear my points. I am in more agreement with you than tatu. Your reasoning is spot on to me and you are correct about over-generalizing a complicated problem (timing the market). In places undergoing intense distressed housing, now might be not a bad time to get your feet wet. However, in most areas like the BA, New York, etc. the local housing market is still in need of adjustments to match the economy.

Tatu's reasoning on the other hand lacks the data and is more about emotion and hope.

Sorry I confused the two threads

This means the bank owns the property until you satisfy the mortgage.

No, it really doesn't. It means you are using the house as collateral until you pay off your loan. If you can't see the difference in those two scenarios, then I'm afraid I can't help you.

Tatu's reasoning on the other hand lacks the data and is more about emotion and hope

What is my reasoning? All I said was that history disputes the false premise that there is a negative correlation between interest rates are prices.

but I'm not willing to spend 20 to 40 years sitting in a cube

Dont worry, nobody will work for the same company for 20 years ever again. The rate of change is so high today, its impossible to see a future.

« First « Previous Comments 93 - 132 of 219 Next » Last » Search these comments

What do you all think? Wait out the Bay Area market a few more years? We have two kids, jobs here and we are renting a 500 square foot home. Should we buy some crap hole under $400,000 in the area, or move to a place where we could have a nice home for $200,000? Should we invest? Please add your reasons why, and any solid data or links you have to help.