A new woe for a pricey housing market: Higher mortgage rates

2018 Apr 18, 9:27am 8,408 views 30 comments

https://www.cbsnews.com/news/a-new-woe-for-a-pricey-housing-market-higher-mortgage-rates/#article

Comments 1 - 30 of 30 Search these comments

1

HeadSet

2018 Apr 18, 12:10pm

HeadSet

2018 Apr 18, 12:10pm

Higher mortgage rates are making the already challenging task of buying an affordable home even tougher for many Americans this spring. ...

A mere extra half percentage point or so can boost monthly payments and add tens of thousands of dollars extra in interest over the life of the typical 30-year loan. At a time when home prices are rising faster than incomes in many parts of the country, that could be enough to shut out some would-be buyers who make the median income in cities such as Seattle and Los Angeles.

Whoa!

Unless you are talking about those few who are paying on variable loans, you are violating Patrick Corollaries 1 and 2:

1. When mortgage rates increase house prices fall. This is a danger to those who bought when interest rates were very low.

2. For the same monthly payment, it is better to have a low price and a high interest rate, rather than a high price and a low interest rate. Makes paying down the loan with extra payments quicker.

For the last few decades, it seemed that mortgage rates and house prices balance to comply with the monthly payment. For example, a $350k house at 4% is about $1670/mo P&I. If rates fall to 3%, that same house price can rise to $395k for about the same P&I. If rates rise instead from 3% to 4%, then the current $395k homes should start falling to an average of $350k.

A mere extra half percentage point or so can boost monthly payments and add tens of thousands of dollars extra in interest over the life of the typical 30-year loan. At a time when home prices are rising faster than incomes in many parts of the country, that could be enough to shut out some would-be buyers who make the median income in cities such as Seattle and Los Angeles.

Whoa!

Unless you are talking about those few who are paying on variable loans, you are violating Patrick Corollaries 1 and 2:

1. When mortgage rates increase house prices fall. This is a danger to those who bought when interest rates were very low.

2. For the same monthly payment, it is better to have a low price and a high interest rate, rather than a high price and a low interest rate. Makes paying down the loan with extra payments quicker.

For the last few decades, it seemed that mortgage rates and house prices balance to comply with the monthly payment. For example, a $350k house at 4% is about $1670/mo P&I. If rates fall to 3%, that same house price can rise to $395k for about the same P&I. If rates rise instead from 3% to 4%, then the current $395k homes should start falling to an average of $350k.

2

GNL

2018 Apr 18, 12:23pm

GNL

2018 Apr 18, 12:23pm

HeadSet says

Not if housing isn't being built. Right now, housing is not being built.

Higher mortgage rates are making the already challenging task of buying an affordable home even tougher for many Americans this spring. ...

A mere extra half percentage point or so can boost monthly payments and add tens of thousands of dollars extra in interest over the life of the typical 30-year loan. At a time when home prices are rising faster than incomes in many parts of the country, that could be enough to shut out some would-be buyers who make the median income in cities such as Seattle and Los Angeles.

Whoa!

Unless you are talking about those few who are paying on variable loans, you are violating Patrick Corollaries 1 and 2:

1. When mortgage rates increase house prices fall. This is a danger to those who bought when interest rates were very low.

2. For the same monthly payment, it is better to have a low price and a high interest rate, rather than a high price and a low interest rate. Makes paying down the loan with extra payments qu...

Not if housing isn't being built. Right now, housing is not being built.

3

LeonDurham

2018 Apr 18, 12:30pm

HeadSet says

Except historically, that's simply not true. It just isn't. Anyone who waits for prices to fall because of interest rates is going to be sad

And it's because housing prices are much more dependent on incomes which tend to be rising when interest rates are high. That effect outweighs the effects of interest rates.

Prices will fall during a recession, however, when rates are low.

When mortgage rates increase house prices fall. This is a danger to those who bought when interest rates were very low.

Except historically, that's simply not true. It just isn't. Anyone who waits for prices to fall because of interest rates is going to be sad

And it's because housing prices are much more dependent on incomes which tend to be rising when interest rates are high. That effect outweighs the effects of interest rates.

Prices will fall during a recession, however, when rates are low.

4

Patrick

2018 Apr 18, 12:36pm

Both are true actually:

1. higher interest rates reduce the price a buyer can pay

2. interest rates tend to rise when the economy is doing well, when people have more money to buy

So it's a timing thing. If rates doubled tomorrow, housing prices would obviously collapse. But if rates rise slowly, trailing the additional money people are getting in raises, then higher rates may not hurt house prices much.

1. higher interest rates reduce the price a buyer can pay

2. interest rates tend to rise when the economy is doing well, when people have more money to buy

So it's a timing thing. If rates doubled tomorrow, housing prices would obviously collapse. But if rates rise slowly, trailing the additional money people are getting in raises, then higher rates may not hurt house prices much.

5

Heraclitusstudent

2018 Apr 18, 12:58pm

Heraclitusstudent

2018 Apr 18, 12:58pm

LeonDurham says

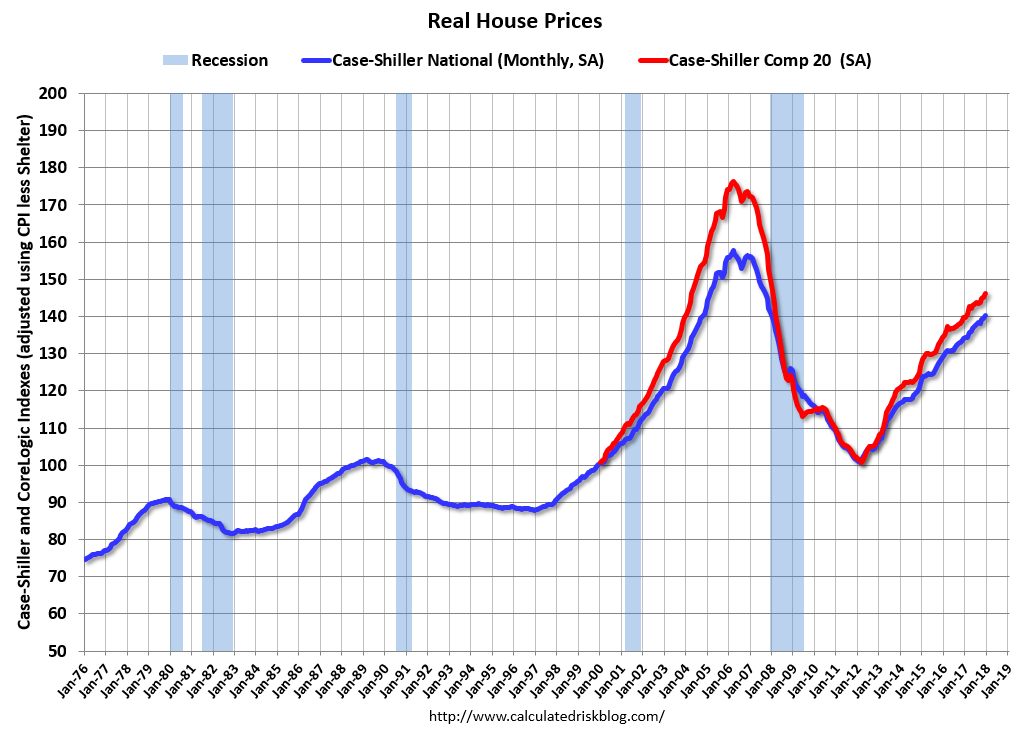

Historically not true? What were prices in real term during the 70s?

We just went through 38 yrs of declining rates. If they start rising now, it matters for all leveraged assets and for p/e ratios in general.

It's a reversal that will ripple through the economy.

Patrick says

Investors won't invest in properties that return 3% when you can get an easy 5% elsewhere without dealing with tenants. Some retired people may sell investment properties to invest somewhere else. Some people may prefer to sell and rent, if they can make more money on their capital somewhere else and cash the difference with the rent.

What rates cannot change is the scarcity of housing.

Except historically, that's simply not true. It just isn't.

Historically not true? What were prices in real term during the 70s?

We just went through 38 yrs of declining rates. If they start rising now, it matters for all leveraged assets and for p/e ratios in general.

It's a reversal that will ripple through the economy.

Patrick says

1. higher interest rates reduce the price a buyer can pay

Investors won't invest in properties that return 3% when you can get an easy 5% elsewhere without dealing with tenants. Some retired people may sell investment properties to invest somewhere else. Some people may prefer to sell and rent, if they can make more money on their capital somewhere else and cash the difference with the rent.

What rates cannot change is the scarcity of housing.

6

FNWGMOBDVZXDNW

2018 Apr 18, 1:16pm

FNWGMOBDVZXDNW

2018 Apr 18, 1:16pm

Many landlords will have a pretty big loan locked in at a low interest rate (3-4%). If house demand started to fall from would be personal use buyers, don't expect landlords to sell at a reduced price. They wouldn't get much if any money back with a sale, so they'd do best to keep their low interest loan and collect rent. The would be buyer may be stuck watching house prices stagnate while interest rates creep up. Their prospective monthly payments for any house purchase will continue to increase, and at a much higher rate if the fed is increasing interest rates. If monthly house payments for purchase are going up fast, expect rents to rise as well. Rents will rise because the other option (buying) is getting more expensive, and they will rise for the same reason that monthly purchase prices are rising. It's because pay will likely be going up in a higher interest rate environment.

7

LeonDurham

2018 Apr 18, 1:18pm

Heraclitusstudent says

In real terms it went mostly sideways, but nobody buys in real terms. I assume when people say prices will fall, they are talking nominally.

Heraclitusstudent says

Of course, but as I stated clearly, it matters less than incomes. And rates rise when incomes are rising.

What were prices in real term during the 70s?

In real terms it went mostly sideways, but nobody buys in real terms. I assume when people say prices will fall, they are talking nominally.

Heraclitusstudent says

We just went through 38 yrs of declining rates. If they start rising now, it matters for all leveraged assets and for p/e ratios in general.

It's a reversal that will ripple through the economy.

Of course, but as I stated clearly, it matters less than incomes. And rates rise when incomes are rising.

8

Malcolm

2018 Apr 18, 2:30pm

Malcolm

2018 Apr 18, 2:30pm

HeadSet says

Correctamundo. The payments didn't change.

For the last few decades, it seemed that mortgage rates and house prices balance to comply with the monthly payment. For example, a $350k house at 4% is about $1670/mo P&I. If rates fall to 3%, that same house price can rise to $395k for about the same P&I. If rates rise instead from 3% to 4%, then the current $395k homes should start falling to an average of $350k.

Correctamundo. The payments didn't change.

9

Heraclitusstudent

2018 Apr 18, 2:38pm

LeonDurham says

Sideways????

Remove the boom and bust and the picture is clear.

Heraclitusstudent saysWhat were prices in real term during the 70s?

In real terms it went mostly sideways,

Sideways????

Remove the boom and bust and the picture is clear.

10

LeonDurham

2018 Apr 18, 2:40pm

Heraclitusstudent says

Not sure I understood your question. But prices went up in real terms during the 70s, not really sideways so I stand corrected.

Sideways????

Remove the boom and bust and the picture is clear.

Not sure I understood your question. But prices went up in real terms during the 70s, not really sideways so I stand corrected.

11

Malcolm

2018 Apr 18, 2:41pm

LeonDurham says

The payment was the same. Interest rates were 18% and a house was about a third of the price as one now. When rates were 8-10%, houses were about half as much, to now when rates are 4% the payment is still pretty much the same. The last housing bailout was simply lowering the interest rates to keep the payment affordable. Nothing really changed. We are still enjoying the benefit of that to this day.

A real world example is a house our family bought in S FL in 1980. It was a $100,000 financed at 12-15% maybe even a little more.

In 2005ish it was worth low to mid $200K. Interest rates were about 7-8%.

It recently sold again in 2015 in the mid $300s. Rates were about 3.75%.

Given the number of remodels and upkeep, I'm going to guess in adjusted dollars it is worth a little less now than it was in 1980, it was new in 1974.

When interest rates rise, housing prices fall in real dollars.

What were prices in real term during the 70s?

In real terms it went mostly sideways, but nobody buys in real terms. I assume when people say prices will fall, they are talking nominally.

The payment was the same. Interest rates were 18% and a house was about a third of the price as one now. When rates were 8-10%, houses were about half as much, to now when rates are 4% the payment is still pretty much the same. The last housing bailout was simply lowering the interest rates to keep the payment affordable. Nothing really changed. We are still enjoying the benefit of that to this day.

A real world example is a house our family bought in S FL in 1980. It was a $100,000 financed at 12-15% maybe even a little more.

In 2005ish it was worth low to mid $200K. Interest rates were about 7-8%.

It recently sold again in 2015 in the mid $300s. Rates were about 3.75%.

Given the number of remodels and upkeep, I'm going to guess in adjusted dollars it is worth a little less now than it was in 1980, it was new in 1974.

When interest rates rise, housing prices fall in real dollars.

12

Goran_K

2018 Apr 18, 2:44pm

Goran_K

2018 Apr 18, 2:44pm

Heraclitusstudent says

Looks pretty clear.

From 2009 to 2013, I think traditionally financed homes were pretty under priced compared to equivalent monthly rents.

Sideways????

Remove the boom and bust and the picture is clear.

Looks pretty clear.

From 2009 to 2013, I think traditionally financed homes were pretty under priced compared to equivalent monthly rents.

13

LeonDurham

2018 Apr 18, 2:46pm

Malcolm says

Except they don't. Look at the 70s in the above chart.

When interest rates rise, housing prices fall in real dollars.

Except they don't. Look at the 70s in the above chart.

14

SFace

2018 Apr 18, 3:22pm

SFace

2018 Apr 18, 3:22pm

Fox plaza, built in 1966. cookie cutter apartment.

https://www.essexapartmenthomes.com/california/san-francisco-bay-area-apartments/san-francisco-apartments/fox-plaza

1/1 600 square feet 12 months lease staring at $4,149 month. Its damn if you buy and damn if you rent.

https://www.essexapartmenthomes.com/california/san-francisco-bay-area-apartments/san-francisco-apartments/fox-plaza

1/1 600 square feet 12 months lease staring at $4,149 month. Its damn if you buy and damn if you rent.

15

Strategist

2018 Apr 18, 4:05pm

Strategist

2018 Apr 18, 4:05pm

HeadSet says

https://www.ocregister.com/2018/04/17/southern-california-house-prices-hit-10-1-2-year-high-realtors-report/

Southern California house prices hit 10 1/2-year high, Realtors report

Winehorror1

"Not if housing isn't being built. Right now, housing is not being built."

1. When mortgage rates increase house prices fall.

https://www.ocregister.com/2018/04/17/southern-california-house-prices-hit-10-1-2-year-high-realtors-report/

Southern California house prices hit 10 1/2-year high, Realtors report

Winehorror1

"Not if housing isn't being built. Right now, housing is not being built."

16

GNL

2018 Apr 18, 4:25pm

Heraclitusstudent says

Bingo, this is the basis for my argument. Basically price meets demand. If housing is not being built, prices will rise rise regardless what rates are or do as long as enough incomes rise.

What rates cannot change is the scarcity of housing.

Bingo, this is the basis for my argument. Basically price meets demand. If housing is not being built, prices will rise rise regardless what rates are or do as long as enough incomes rise.

17

lostand confused

2018 Apr 18, 5:01pm

lostand confused

2018 Apr 18, 5:01pm

APOCALYPSEFUCKisShostikovitch says

In some areas yes. Here is this decent house in Detroit, MI for 8,500 bucks -5 bedroom 2 bath!

Does need TLC, windows-, back taxes etc-but can find plenty of these homes there?

https://www.realtor.com/realestateandhomes-detail/2911-Virginia-Park-St_Detroit_MI_48206_M46679-67127

I wonder if IL is facing this because of high property taxes and the fleeing hordes from the dem policies?

Housing is practically free in the states.

.

In some areas yes. Here is this decent house in Detroit, MI for 8,500 bucks -5 bedroom 2 bath!

Does need TLC, windows-, back taxes etc-but can find plenty of these homes there?

https://www.realtor.com/realestateandhomes-detail/2911-Virginia-Park-St_Detroit_MI_48206_M46679-67127

I wonder if IL is facing this because of high property taxes and the fleeing hordes from the dem policies?

18

Malcolm

2018 Apr 18, 5:39pm

LeonDurham says

The chart doesn’t include the rates but I see the pattern. The late 70s show a decline. I never said there wasn’t a lag, the graph clearly shows a relationship in price to interest rates in general. Even the fluctuations correct with time.

Except they don't. Look at the 70s in the above chart.

The chart doesn’t include the rates but I see the pattern. The late 70s show a decline. I never said there wasn’t a lag, the graph clearly shows a relationship in price to interest rates in general. Even the fluctuations correct with time.

19

Malcolm

2018 Apr 18, 5:42pm

WineHorror1 says

Interest rates follow income levels. Both by monetary policy and by a demand for investment capital and inflation.

Bingo, this is the basis for my argument. Basically price meets demand. If housing is not being built, prices will rise rise regardless what rates are or do as long as enough incomes rise.

Interest rates follow income levels. Both by monetary policy and by a demand for investment capital and inflation.

20

LeonDurham

2018 Apr 19, 6:07am

Malcolm says

The late 70s show a rise in real home price index from ~75 to 90 while interest rates were going from 9% to 16%. There is no decline there so I'm not sure what you're looking at. The decline starts when the US goes into recession in 1980.

There are charts of interest rates vs. home prices and it's a slightly positive correlation (home prices rise when rates rise and fall when rates fall) but it's so weak as to be basically no correlation.

The chart doesn’t include the rates but I see the pattern. The late 70s show a decline. I never said there wasn’t a lag, the graph clearly shows a relationship in price to interest rates in general. Even the fluctuations correct with time.

The late 70s show a rise in real home price index from ~75 to 90 while interest rates were going from 9% to 16%. There is no decline there so I'm not sure what you're looking at. The decline starts when the US goes into recession in 1980.

There are charts of interest rates vs. home prices and it's a slightly positive correlation (home prices rise when rates rise and fall when rates fall) but it's so weak as to be basically no correlation.

21

Shaman

2018 Apr 19, 7:27am

Shaman

2018 Apr 19, 7:27am

My home was 3/4 million, way outside the affordable range for most middle class families. And yet, various factors combined to make it affordable for my family. A previous purchase which appreciated got us a nice down payment to use on this one. And my wife going back to work after having and raising our three kids to school age brought our income to a fairly high level. All of a sudden what was completely unaffordable became a piece of cake because we broke two of the traditional metrics: 1) high down (and this is normally being supplied around here by parents with money), 2) dual income rather than single income.

Point is: don’t write off housing as too expensive because traditional metrics don’t work on it. In places where it’s scarce, people will find a way to buy.

Point is: don’t write off housing as too expensive because traditional metrics don’t work on it. In places where it’s scarce, people will find a way to buy.

22

NDrLoR

2018 Apr 19, 8:50am

NDrLoR

2018 Apr 19, 8:50am

LeonDurham says

The late 70s show a rise in real home price index from ~75 to 90 while interest rates were going from 9% to 16%. There is no decline there so I'm not sure what you're looking at. The decline starts when the US goes into recession in 1980.The 70's was an aberration, plagued with hyper-inflation compared to previous decades. For instance, automobile prices, the biggest expense before a home, increased 110% between 1970 and 1980--it had been about 13% between 1960 and 1970. The same huge increases were observed in the housing market of the decade. The double digit interest rates finally choked off runaway inflation, but at the expense of one of the worst recessions in the postwar era after the one of 1973-1975, so there was no place for the prices to go but down once inflation was reigned in.

23

LeonDurham

2018 Apr 19, 8:58am

P N Dr Lo R says

Not really. It was comparatively high inflation, to be sure. But not an aberration.

That time period clearly shows that home prices follow wages much more closely than they follow interest rates.

The 70's was an aberration, plagued with hyper-inflation compared to previous decades.

Not really. It was comparatively high inflation, to be sure. But not an aberration.

That time period clearly shows that home prices follow wages much more closely than they follow interest rates.

24

Strategist

2018 Apr 19, 9:15am

Quigley says

They always have.

Point is: don’t write off housing as too expensive because traditional metrics don’t work on it. In places where it’s scarce, people will find a way to buy.

They always have.

25

Strategist

2018 Apr 19, 9:16am

Quigley says

They always have.

Point is: don’t write off housing as too expensive because traditional metrics don’t work on it. In places where it’s scarce, people will find a way to buy.

They always have.

26

Malcolm

2018 Apr 19, 9:40am

LeonDurham says

I said in a different part that there is lag. People don''t just sell a fixed rate house when interest rates rise, but when they do go to sell it affects it on the demand side, just like the graph shows.

There are many things that affect the short time price changes in real estate. For one thing, as demand drops off, the median price of actual sales stays high, and even can rise in a misleading way. Speculators following an upward trend will overpay in relation to basic fundamentals, including mortgage rates, that's how bubbles form. Then you have a correction or a crash.

In some areas where houses are dirt cheap and mortgages play little effect on the price, the prices tend to be very level. Mortgage rates clearly affect the present value of a pricier house. Wage inflation will have a similar effect to lowering interest rates, but wage inflation leads to higher interest rates. They kind of cancel out.

If I am wrong, then why did the government start lending money at zero to sustain home prices? Inflation has led to home prices being slightly higher than the last bubble but if interest rates go back to 8% with all things being equal, I would bet that houses would fall by 50%.

The late 70s show a rise in real home price index from ~75 to 90 while interest rates were going from 9% to 16%. There is no decline there so I'm not sure what you're looking at. The decline starts when the US goes into recession in 1980.

I said in a different part that there is lag. People don''t just sell a fixed rate house when interest rates rise, but when they do go to sell it affects it on the demand side, just like the graph shows.

There are many things that affect the short time price changes in real estate. For one thing, as demand drops off, the median price of actual sales stays high, and even can rise in a misleading way. Speculators following an upward trend will overpay in relation to basic fundamentals, including mortgage rates, that's how bubbles form. Then you have a correction or a crash.

In some areas where houses are dirt cheap and mortgages play little effect on the price, the prices tend to be very level. Mortgage rates clearly affect the present value of a pricier house. Wage inflation will have a similar effect to lowering interest rates, but wage inflation leads to higher interest rates. They kind of cancel out.

If I am wrong, then why did the government start lending money at zero to sustain home prices? Inflation has led to home prices being slightly higher than the last bubble but if interest rates go back to 8% with all things being equal, I would bet that houses would fall by 50%.

27

Malcolm

2018 Apr 19, 9:42am

Strategist says

There is also that phenomenon. It used to be that a couple would buy a three bedroom house and have children. Now a three bedroom house can be a three family house of couples with maybe one child in the house.

Point is: don’t write off housing as too expensive because traditional metrics don’t work on it. In places where it’s scarce, people will find a way to buy.

There is also that phenomenon. It used to be that a couple would buy a three bedroom house and have children. Now a three bedroom house can be a three family house of couples with maybe one child in the house.

28

Patrick

2018 Apr 19, 9:45am

SFace says

This generally true in the Bay Area. Venture capital transfers vast sums from their investors to local landlords via programmer salaries. But buying is no better, and often worse, for the same reason.

lostand confused says

Have you been to Detroit? The house may look nice, but the danger is extreme. There is pervasive and violent anti-white racism which makes it a bad idea for white people to visit there, much less move there. The few white people in Detroit are generally Lebanese (both Christians and Muslims) who came from a literal war zone and so are not all that freaked out by gunfire and beatings. Here is about as positive a spin as you can put on it: http://streetcarnage.com/blog/being-white-in-detroit/

Its damn if you buy and damn if you rent.

This generally true in the Bay Area. Venture capital transfers vast sums from their investors to local landlords via programmer salaries. But buying is no better, and often worse, for the same reason.

lostand confused says

Here is this decent house in Detroit, MI for 8,500 bucks -5 bedroom 2 bath!

Does need TLC, windows-, back taxes etc-but can find plenty of these homes there?

Have you been to Detroit? The house may look nice, but the danger is extreme. There is pervasive and violent anti-white racism which makes it a bad idea for white people to visit there, much less move there. The few white people in Detroit are generally Lebanese (both Christians and Muslims) who came from a literal war zone and so are not all that freaked out by gunfire and beatings. Here is about as positive a spin as you can put on it: http://streetcarnage.com/blog/being-white-in-detroit/

29

Strategist

2018 Apr 19, 9:58am

Malcolm says

People will downsize if they have no choice, like sharing a house. They can get a smaller home, a condo, a cheaper neighborhood, or move to the boonies.

Sadly, not many choices.

Strategist saysPoint is: don’t write off housing as too expensive because traditional metrics don’t work on it. In places where it’s scarce, people will find a way to buy.

There is also that phenomenon. It used to be that a couple would buy a three bedroom house and have children. Now a three bedroom house can be a three family house of couples with maybe one child in the house.

People will downsize if they have no choice, like sharing a house. They can get a smaller home, a condo, a cheaper neighborhood, or move to the boonies.

Sadly, not many choices.

30

LeonDurham

2018 Apr 19, 10:45am

Malcolm says

Graphs of housing prices vs. interest rates don't show negative correlation even with whatever lag you want to add.

It doesn't make sense anyway. Interest rates rose for 3 years before house prices starting falling in 1980. You think it's a 3 year lag?? On the other hand, the beginning of the housing price decline corresponded very closely with the recession and incomes falling.

Malcolm says

I'm not sure exactly what you are arguing, so I can't say definitively that you are wrong. Government absolutely tries to lower interest rates during a recession to spur investing. Buying a house is one facet of that.

I'm just saying historically rates doubling hasn't cause housing to fall by 50%. On the contrary, it has actually correlated with housing price increases. And this is because interest rates don't rise in a vacuum. There is almost always income rise going along with it, and the income rise drowns out any effects of the interest rate.

I said in a different part that there is lag. People don''t just sell a fixed rate house when interest rates rise, but when they do go to sell it affects it on the demand side, just like the graph shows.

Graphs of housing prices vs. interest rates don't show negative correlation even with whatever lag you want to add.

It doesn't make sense anyway. Interest rates rose for 3 years before house prices starting falling in 1980. You think it's a 3 year lag?? On the other hand, the beginning of the housing price decline corresponded very closely with the recession and incomes falling.

Malcolm says

If I am wrong, then why did the government start lending money at zero to sustain home prices? Inflation has led to home prices being slightly higher than the last bubble but if interest rates go back to 8% with all things being equal, I would bet that houses would fall by 50%.

I'm not sure exactly what you are arguing, so I can't say definitively that you are wrong. Government absolutely tries to lower interest rates during a recession to spur investing. Buying a house is one facet of that.

I'm just saying historically rates doubling hasn't cause housing to fall by 50%. On the contrary, it has actually correlated with housing price increases. And this is because interest rates don't rise in a vacuum. There is almost always income rise going along with it, and the income rise drowns out any effects of the interest rate.

patrick.net

An Antidote to Corporate Media

1,352,789 comments by 15,729 users - HANrongli, HeadSet, RWSGFY, WookieMan online now