patrick.net

An Antidote to Corporate Media

1,350,937 comments by 15,722 users - HeadSet, Hf online now

« First « Previous Comments 46 - 85 of 125 Next » Last » Search these comments

Just by asking what these fundamentals are, I can tell you didn’t know this. So maybe next time you are actually curious and want me to explain it to you in a way that isn’t rude, you don’t shoot the question at me like a complete fucking prick yourself. OK?

I’m not curious as to what you think. I’m curious as to how you can walk through the front door with such a large head.

If you don’t want to be treated like a “complete f’ing prickâ€, stop acting like one.

This is my first time here and I'm new to the US real estate market so I'm trying to learn what I can where I can. Klarek, I suspect that someone here has more than one account and is using different names to offer himself "public" support. I completely understand what you're saying. I've been looking to buy a house and in the last two weeks, about 75% of all the houses I've been looking at have had price reductions. Many are being re-posted under different MLS numbers. With millions more foreclosures in the works, and fewer and fewer people able to buy, I don't see how prices can go anywhere BUT down. I've decided to watch and wait for a while longer.

So the majority of US metro areas didn’t fall then, right?

Read between the lines. The article reports sales activity has dropped "25% from the previous year." That's a 25% drop from a BAD year. Without adequate sales activity, the excessive inventory cannot be removed from the market. Also, banks are withholding literally millions of REOs from the market so as not to swamp an already bloated market. Furthermore, every day that goes by, more properties are being added to the shadow inventory via foreclosures, adding further downward pressure in the future to prices once these properties are forced into the market.

Keep in mind also that this inventory is not being diminished with record low fixed rate mortgages. What happens when interest rates are eventually forced up?

Keep in mind also that this inventory is not being diminished with record low fixed rate mortgages. What happens when interest rates are eventually forced up?

If history is any guide, then prices will be rising...

If history is any guide, then prices will be rising…

Interest rates have historically been PUSHED up by the Fed, never forced up by the macro situation.

The current Ireland and Greece case is a bit different from Volcker in 1979.

If history is any guide, then prices will be rising…

Interest rates have historically been PUSHED up by the Fed, never forced up by the macro situation.

The current Ireland and Greece case is a bit different from Volcker in 1979.

http://research.stlouisfed.org/fred2/series/MORTG/

I agree--this time might be different. Just usually it isn't...

We’re not even halfway to terminal velocity.

Prepare for housing prices not seen since 1977.

Then total economic collapse.

Housing speculators will be burning their empty buildings, even with Section 8 tenants in them, to uncover earth they can use to plant potatoes.

The entire country has been deindustrialized and the high-paying craft work jobs are all in slave states like China. All of the displaced workers ended up in part time jobs at WalMart, on the streets, dead or in one way or another speculating in real estate. No one in their right mind will buy a building as an investment in the next three generations if civil societies don’t crumble and if the US doesn’t devolve into a feudal dystopia of disconnected warlord states.

The best we can hope for is a long-term economic collapse. The worst is collapse, followed by civil war and the rise of theocratic warlord states, led by Jesufascist end-timers.

Plant potatoes and teach wife and kids how to handle light and heavy ordnance.

Man, I've been missing a lot of fun since I bought my house in January.

I hate to break it to the DOOM soothsayers, but your stacking your chips to bet against the free world's most powerful government. QE2 is already inflating us out of our debt hole and re-engergizing the economy. You need to break away from the sheep and start running with the wolves.

We are at the cusp of America's largest economic boom in the history of human economic booms. Hold on tight because the BOOMers are here!

I agree–this time might be different. Just usually it isn’t…

Every time is different. The America of 1800, 1850, 1900, and 1950 was under-developed and needed more labor to get business rolling.

Today, not so much, and we have trained about two billion offshore people to do many of our wealth-creating jobs for $10/day, if that.

Income disparities are more like 1929 than 1949. Credit cannot bridge this gap permanently.

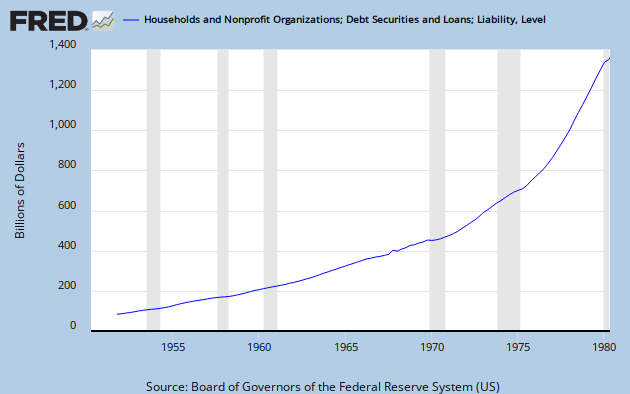

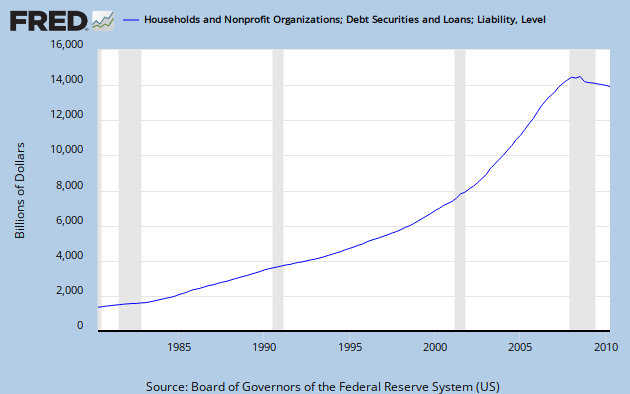

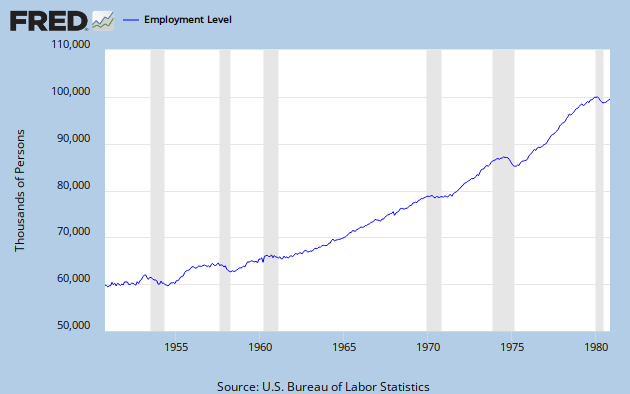

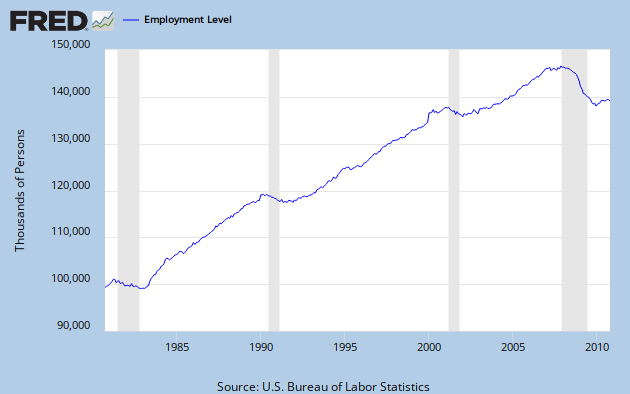

Hmm. Here's two charts:

{kind=link}

{kind=link}

While they look very similar, I think the underlying dynamics are very different. The bump in 1973-1979 may have been due to the baby boom -- and women -- entering the work force en masse. There was of course high inflation during this time, the minimum wage doubled from $1.60 to $3.35, 1970 to 1981.

Wages didn't double 2000-2010, that's for sure. Neither did employment.

{kind=link}

{kind=link}

yep, deficit spend and nationalize the debt to start off a boom!!!

its working so well in greece, ireland, iceland!!! what could go wrong?

You have it backwards. Greece, Ireland, Iceland did not nationalize debt before the collapse. They nationalized as a consquence.

Businesses do this all the time. Credit is used during the lean times to float until the flush times. Retailers don't even hit the black until Black Friday.

You can't throw your citizens overboard during the down business cycles (although the Tea Party is working as hard as hell to euthanize "worthless" people getting government help). They forget that these are the same people needed when the economy booms.

If we are worse of than Ireland, it is because of our endless wars of occupation in Iraq and Afghanistan.

Every time is different.

Yes and no. If you look hard enough you'll find differences. But I think some general trends stay remarkably similar.

C-S's August numbers are 93.57, 100.76, 113.58 for the three tiers.

This is 1.3%, 0.2%, and 2.9% above the March-May 2009 low.

C-S’s August numbers are 93.57, 100.76, 113.58 for the three tiers.

This is 1.3%, 0.2%, and 2.9% above the March-May 2009 low.

Should C-S the sole tool to gauge home prices?

http://seekingalpha.com/article/228271-housing-wise-to-look-beyond-case-shiller-index

http://www.zerohedge.com/article/why-case-shiller-index-although-showing-another-downturn-coming-overly-optimistic-and-quite-

Well I am renting now, and am ready for prices to drop. I've been saving funds, so interest rate won't matter as much to me (relatively speaking).

The most recent Zillow report is also extremely negative. We have reached a new record percentage of "owners" who are underwater. Nice. It is true that total collapse zones such as Las Vegas (currently a full 80% of "owners" are underwater) influence the statistic, but even places such as my home (MN) are adding to the downward spiral. Zillow has my exurb at a -10% Y-O-Y. According to the CS data, Minneapolis is right up there at the top of the list for "apprecation" after SF and SD - the only problem is that once you include ALL sales, not just single-family homes, the prices were NEGATIVE (-3.5%). I am looking at the article right now. Additionally, losses have quickly intensified after the credit expired. I see zero evidence any bottom has been hit locally despite the statistical mirage that is the Minneapolis CS data. Sales are so low do prices paid even matter to the general market? It's difficult to say.

http://zillow.mediaroom.com/index.php?source=patrick.net&s=159&item=215#wd_printable_content

I put an offer in for a short sale for $400k. They stalled out for over a year before I gave up. A year later, they listed the house for $399k! They just reduced it to $299k. I don't think short sales are for selling the homes, but to manipulate the owner into continual payments. The list price usually a big joke.

The short sale was in Raleigh, NC. We aren't having as much drama here as the west coast, but we are seeing it start to happen. Eventually, it will be felt everywhere.

I just got one of my short sales approved this morning!

Last sale: 97K in 2004…

My contract: 42K.

Nice. How much can you rent that out for? How are the HOAs in AZ? I know you probably don't want to give specifics, but what area of AZ is that in? Thanks.

October CS data measured June through August. You bet your ass there was some tax credit-fueled demand that closed within that time frame

Your friend Roberto disagrees with you. This is what he says on a different thread.

"good grief! sales number tell us how many people are buying now! of course this gives us an idea of current, or worst case, 45 day ago, demand. "

He thinks worst case is 45 day closings unless I'm misinterpreting him.

So, my argument is that prices rose when the tax credit was in place, and STOPPED rising when the tax credit ended, which proves your statement false.

You need some pointers on cause and effect. You may assume that the tax credit was the cause, but you're far from PROVING it.

So, my argument is that prices rose when the tax credit was in place, and STOPPED rising when the tax credit ended, which proves your statement false.

You need some pointers on cause and effect. You may assume that the tax credit was the cause, but you’re far from PROVING it.

Ha ha. *I* need some pointers, eh? So then it is your contention that the price increase that coincides with the beginning of the tax credit, the dip that coincides with the original expiration of the tax credit, and the second increase that coincides with the extension of the tax credit, are all utterly coincidental?

It's quite obvious that this could NEVER be proven to YOUR satisfaction.

Good post klarek. here's a more complete report from Clear Capital. Its as if they read this Forum and answered directly!

http://clearcapital.com/company/MarketReport.cfm?month=November&year=2010

The REO Saturation numbers look preposterous. 61% REO Saturation for ATL? What does that even mean? 61% of the homes on the market? ???

So, my argument is that prices rose when the tax credit was in place, and STOPPED rising when the tax credit ended, which proves your statement false.

You need some pointers on cause and effect. You may assume that the tax credit was the cause, but you’re far from PROVING it.

What in the world makes you think that they will start rising again? I would like a somewhat sophisticated or educated reason that they would go from a 6% drop in two months to an all-of-a-sudden rise during winter. Please enlighten/amuse me.

Ha ha. *I* need some pointers, eh? So then it is your contention that the price increase that coincides with the beginning of the tax credit, the dip that coincides with the original expiration of the tax credit, and the second increase that coincides with the extension of the tax credit, are all utterly coincidental?

It’s quite obvious that this could NEVER be proven to YOUR satisfaction

I'm not sure how the dip that coincides with the original expiration helps your case at all. The credit never actually expired--it was extended before the original expiration date. So, please tell me exactly how the scenario works in your world?

Anyways--I agree that sales activity and prices probably will fall for a few months after the credit ends. Like I've said many times--the credit surely pulled foward some demand. Whether it will be short dip or continuation of the downturn isn't clear to me yet.

What in the world makes you think that they will start rising again? I would like a somewhat sophisticated or educated reason that they would go from a 6% drop in two months to an all-of-a-sudden rise during winter. Please enlighten/amuse me.

Did I say they will start rising again during winter?? No. But I do think there is a reasonable chance it will be a short dip followed by flat to slowly rising prices (seasonally adjusted). Read my previous post for the explanation.

It will depend on the overall economy. If unemployment continues to fall, then the housing should be OK.

Ha ha. *I* need some pointers, eh? So then it is your contention that the price increase that coincides with the beginning of the tax credit, the dip that coincides with the original expiration of the tax credit, and the second increase that coincides with the extension of the tax credit, are all utterly coincidental?

It’s quite obvious that this could NEVER be proven to YOUR satisfaction

I’m not sure how the dip that coincides with the original expiration helps your case at all. The credit never actually expired–it was extended before the original expiration date. So, please tell me exactly how the scenario works in your world?

I believe the original expiration date was to CLOSE the contract, so no, by the time they announced an extension, the time to enter escrow had already passed. I distinctly remember a period where we did not know if the credit would be extended, don't you?

Looking up sources to prove a point to the idiot duck isn’t high on my agenda

Yes. I know. Looking up sources isn't high on your list... Unfortunately, it doesn't stop you from posting nonsense.

Anyone else seeing the job market heating up big time? Just ate with a headhunter who said it was hottest he's seen in six years. Same everywhere?

Anyone else seeing the job market heating up big time? Just ate with a headhunter who said it was hottest he’s seen in six years. Same everywhere?

Yeah right! LOL.

Anyone else seeing the job market heating up big time? Just ate with a headhunter who said it was hottest he’s seen in six years. Same everywhere?

anecdotal evidence isn't really helpful in giving an overview of the health of the overall market.

software engineers have been recruited heavily by facebook, google, and even startups for the last year.

anything to do with construction is dead.

you really have to go by unemployment/underemployment numbers to get an overview.

..could be that unemployed have now a feeling that the new congress will limit UE to 99 weeks, hence take whatever to pay the bills. That has nothing to with housing recovery. Housing recovery needs well paid jobs back...now that easy loan days are gone....figure it out ..which way the housing is heading.

Uh…he said 5-10 years.

In Japan, there has been 20+ years now and still no new real-estate bubble.

Possibly obscure side note: ch_tah doing any galloping lately?

What about the FED Factor ? I think FED is on a mission to devalue dollar/pump up the stock/real estate market.

I don't think any thing can stop the FED at this point. I don't think any political entity will stop the FED. Some of politicians will pretend they are trying to stop this. But they really won't. They all know the inflation is inevitable. That's the only way out of this without the big bank casualties.

Then the question, for a middle class like me, is how does this timing of inflation plays against the future house prices ????

What about the FED Factor ?

What about it?

Economies experience inflation via a combination of "animal spirits" -- confidence in the future -- and the credit cycle converting savings into cash via the exercise of credit.

The Fed is dumping $600B in the banking system -- $100B per month -- next year. If we had a normal credit cycle this new capital would expand into maybe $6T of bank-money as fractional-reserve banking distributed it through the system.

But bank-money is not cash. Every loan has to come from somebody's savings in the bank. It's only when people are parking money in the bank that banks can expand the money supply through lending, as loans ping-pong through checking accounts, into savings, and back out as loans.

But these days, nobody solvent right now really needs to take on any more debt -- there's no demand.

Things were much different with the 2003-2007 credit boom, then, the rising home valuations were liberating $100B/month or so in new cash money as people cashed out their equity and spent it.

http://research.stlouisfed.org/fred2/series/CMDEBT

What the Fed is doing now is just fighting the gravitational pull of a deflationary collapse, since the 2004-2007 bubble valuations are gone now, leaving debt and sky-high under employment.

The situation is highly analogous to the Japan experience. We got a bit ahead of ourselves economically, 2004-2007, and now the bill is due, with interest.

We can't cut government jobs

http://research.stlouisfed.org/fred2/series/USGOVT

that's the only sector that has expanded since 2000.

We can't raise taxes to reduce trillion-dollar deficit since that will drive rich people out of the country or into their secret hideouts and they will stop being the great Captains of Industry we so desperately need.

{kind=link}

The end result of all this bullshit is just going to be more and more money moving into the wealthy's pockets and the middle class and below getting entirely screwed. That's the playbook for the next two years, the American people really don't know how crazy-bad it's going to get. We're talking Bachmann crazy here.

and what things are going up in price? commodities, not salaries

Plus it will go into asset buys here in the states. Everybody expects CPI inflation to hit here someday, and stuff looks pretty cheap if you've got $500M or more to throw into the market and can wait several years for the inflation man to come.

Social Security Agency's Chief Actuary is working with the following assumptions of wage inflation:

2020 +17.3% from 2010

2030 +30.9%

2040 +47.4%

2050 +65.3%

2060 +85.2%

2070 +106.9%

ie, wages will double by 2070. 20% is about what wages have grown since 2000, but it remains to be seen how sticky these wages are.

The situation is highly analogous to the Japan experience. We got a bit ahead of ourselves economically, 2004-2007, and now the bill is due, with interest ....

That’s the playbook for the next two years, the American people really don’t know how crazy-bad it’s going to get. We’re talking Bachmann crazy here.

You seem to contradict yourself here.

If we are tracking the Jap. experience, not much bad has happened to their middle class: in fact, many who couldn't reasonably afford their own home previously got one now and many have improved their living situation beyond their expectations.

So what specifically crazy-bad you expect in the next 2 years? I think the line for next 2 years (not much happening really) is largely fixed by recent elections, and any change (whether good or bad) is delayed till 2013.

not much bad has happened to their middle class

Don't mistake Tokyo for the rest of the country, and don't mistake middle-class "salarymen" for the population as a whole. The employment rate for Japan is at an all-time low, ~56%.

Hours are down, wages are down:

half of women workers are temps.

http://www.stat.go.jp/english/data/handbook/c12cont.htm#cha12_4

I think the line for next 2 years is largely fixed by recent elections,

And that's the problem. The Republicans have this strange idea that stimulus "must be paid for", ie we have to cut government spending somewhere before government can spend somewhere else!

That's a pretty bizarre idea for stimulus. And not being able to raise taxes any more is going to put the entire USD and our sovereign debt rating at some degree of systemic risk a la Greece. Our sovereign debt CDS is already less than pristine now.

Now, I don't know anything really and I'm just talking through my hat here, but I don't think things are going to get any better in the next two years. QE2 might bring us some inflation in commodities, but that's only good for farm belt, and comes at the risk of inflation in energy costs, which the farm belt is highly sensitive to.

Hours are down, wages are down:

So wages decreased by ~10% over 15 years. But RE prices dropped ~2 - 5 times depending on location, right? The RE costs decreased even more drastically, due to lower mortgage rates. Many other prices also decreased, many by 10% or more. I'd beg for a 10% pay cut any day, if 1 M houses drop to 200 - 500 K while the mortgage rate becomes ~2.5%.

But RE prices dropped ~2 - 5 times depending on location, right?

~35%, actually, 1995-2008.

http://www.nuwireinvestor.com/articles/the-state-of-japans-real-estate-market-53959.aspx

from the peak prices, maybe 50% in Tokyo:

I’d love a pay cut of 10% any day, if 1 M houses dropped to 200 - 500 K while the mortgage rate became ~2.5%

The problem with this scenario is you've got to be the person with a job still. And prices are still pretty whack compared to rents. And Japan is running a national debt at ~200% of GDP, with a declining population, and diminishing competitive advantage vs. China.

I have no idea what's going to happen with Japan this century, but I'd like I've said before I'd rather have our problems than theirs. All our problems can be fixed by taxing the shit out of the rich (like everyone else does) and instituting profit controls on medicine (again, like everyone else does). But nooo, our precious snowflake wealthy people will run off to Paraguay if marginal rates go over 40% again and our doctors will run to Mexico to escape onerous cost controls on their practices.

US Mortgage Applications Hit 4-Month Low - http://www.cnbc.com/id/40230256/

...and before you waste my time making up excuses for it - yes, it IS seasonally adjusted, bitchez.

« First « Previous Comments 46 - 85 of 125 Next » Last » Search these comments

5.9% drop in US home prices in two months!!!

http://www.clearcapital.com/company/pr_details.cfm?source=patrick.net&position=30686#header