Thread for orphaned comments

2005 Apr 11, 5:00pm 232,896 views 117,730 comments

by Patrick ➕follow (59) 💰tip ignore

« First « Previous Comments 2,278 - 2,317 of 117,730 Next » Last » Search these comments

we looked at a lot of "Needs TLC. Fixer. Diamond in the rough. build sweat equity. " houses... most were tear-downs or in need of a complete gut/remodel

A tear down, really? Is it infested with termites or condemned due to mold? Seriously, unless it's condemned for some environmental reasons I doubt really a "tear down". Our house wasn't touched since 1949 except the roof, which was leaking...it was nowhere near a tear down, nothing that a roof, gutters, paint and flooring didn't fix.

It's funny how when it's a house you buy in the area for too much money it's a light fixer. When it's a house that shows prices are still falling, it's a tear down.

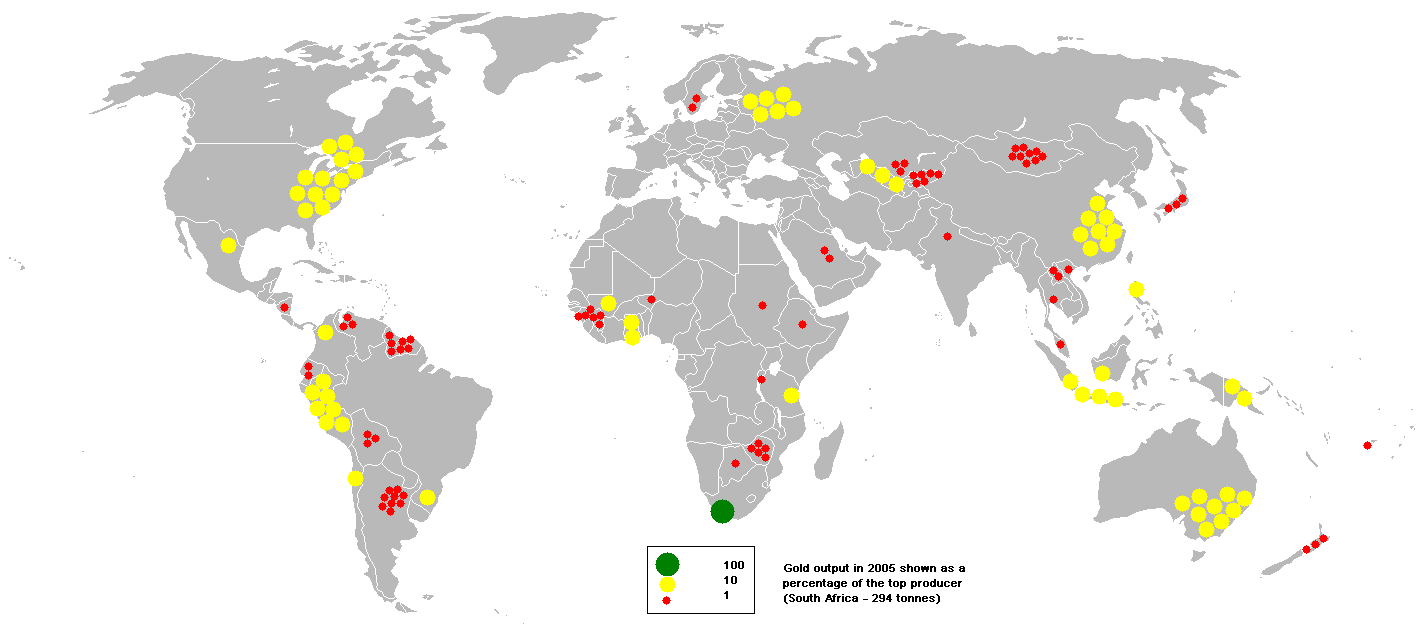

Exactly how much gold do we have Oakman? Last I recall we haven’t even done a physical account of the storage in Fort Knox in decades. There’s also quite a bit on ZeroHedge about the Gold ETF having pretty much no direct connection to actual physical gold. I have read that the entire world above-ground gold amounts to about 20 cubic meters. Looking at this chart:

We don’t seem to have very many highly-productive mines.

I'm assuming it's still in Fort Knox and the Fed isn't lying about it's balance sheet. As far as GLD, GLD does has tons of physical in vault. They just don't have enough to pay out the holders of GLD.

Forgive me for jumping in with all that preceded this. I've only scanned through the comments. My question is "how much of this is mental?" I had that discussion with a sub-vendor of mine earlier today. Everyone wants to believe that things will go up to, but few are willing to put their $$$ where their mouth is. Many RFQ's, few orders. The bottom line is we are all "cautiously optimistic" but no one is willing to make that fist move into the unknown. If suddenly we collectively say "the worst is over, it's save to spend again" then things will stake off, and we will have two - three years of growth, and "recovery" independent of the fundamentals behind said growth. In short believing things will get better is almost as good as things actually getting better.

If suddenly we collectively say “the worst is over, it’s save to spend again†then things will stake off, and we will have two - three years of growth, and “recovery†independent of the fundamentals behind said growth. In short believing things will get better is almost as good as things actually getting better.

This assumes the collective in question is entirely comprised of savers with stable employment/stable and/or growing salaries, all waiting to spring from the sidelines. I don't see that, for the most part. You cannot spend what you don't have, and what the banks aren't lending, and I think the money-for-nothing paradigm is a thing of the past.

I guess the question is - why would anyone fork over 1850 a month in rent when they could buy the same property with zero down for what you paid and have less overhead every month? It doesn't make good sense - unless, of course, your renters are on a temporary contract or something.

pkennedy and thomas,

Well here is how I look at it.

50/50 change, either I meet the dinosaur on the street or not (c. joke)

But if what's the worst case scenario: for me, is that it is a double dip. Hence I'd rather wait it out for example.

It is all a matter of perception, is the cup half full or half empty.

You both looking it at it from two opposite directions.

I think I am with thomas, because if dips the 2nd time I can be screwed. If it does not, well, for now I will save, and will have ability to put an even bigger down payment (dollar and % wise to cover), but risk will be less.

Just my 2 cents

I’m assuming it’s still in Fort Knox and the Fed isn’t lying about it’s balance sheet.

Fort Knox has not has an audit for over 50 years. As far as the Fed is concerned, to the best of my knowledge, they've never had an audit. As far as "lying" by the Fed? I'm sure that they are absolutely trustworthy and would never, ever deceive anyone.

Interesting, "no cars on the street" policy. So If it is a 4/2 house where there are two adults and 1 kid over 18, i.e. 3 cars in the household, where should they store their 3rd car (provided there is space carport or garage for two cars)

As far as rent for 1800, well, area is not so great in that part of Concord. I can see how renters credit may not be so good either, hence they are somewhat forced to pick this community over living in an apartment for example.

You can't get 100% financing on investment properties, more like 75%, and only then if your ratios and credit score are pristine. Claiming that, puts the BS meter on high for one poster on this thread, its been a good while since any bank would offer anything close to that.

OK, I’ll ask you a question. How did the world operate when we WERE on the gold standard? Low inflation, fiscal responsibility, no currency debasing? I don’t know - thats sounds good to me.

You are perhaps somehow not aware that there was a major financial crises in America roughly every 20 years from the signing of the Declaration of Independence up to and including the great depression. Here are some hints:1797, 1819, 1837, 1857, 1873, 1893, 1901, 1907. These were just the biggies, there were smaller economic hiccups also. Widespread business collapses, stock market collapses, massive bank failures, high poverty, 20% unemployment, credit collapse, real estate collapses, high foreclosures. All of which happened on the gold standard. Sounds familiar to me. Explain again how this is utopia.

Rose colored glasses are always a good thing. Nothing changes.

So why is it that the DOLLAR has gone into a death spiral since the US has went off the gold standard in 1973?

How is it again that inflation, fiscal irresponsibility, deficit spendig, and the debasing of our currency is a good thing? Nothing changes, the result is always the same, economic chaos. Well -DAH.

OK, I’ll ask you a question. How did the world operate when we WERE on the gold standard? Low inflation, fiscal responsibility, no currency debasing? I don’t know - thats sounds good to me.

You are perhaps somehow not aware that there was a major financial crises in America roughly every 20 years from the signing of the Declaration of Independence up to and including the great depression. Here are some hints:1797, 1819, 1837, 1857, 1873, 1893, 1901, 1907. These were just the biggies, there were smaller economic hiccups also. Widespread business collapses, stock market collapses, massive bank failures, high poverty, 20% unemployment, credit collapse, real estate collapses, high foreclosures. All of which happened on the gold standard. Sounds familiar to me. Explain again how this is utopia.

Rose colored glasses are always a good thing. Nothing changes.

Well, fractional reserve banking is an abandonment of the gold standard. It should be illegal. All these banking crises that you speak of are a symptom of paper money being substituted for gold.

I’m assuming it’s still in Fort Knox and the Fed isn’t lying about it’s balance sheet.

Fort Knox has not has an audit for over 50 years. As far as the Fed is concerned, to the best of my knowledge, they’ve never had an audit. As far as “lying†by the Fed? I’m sure that they are absolutely trustworthy and would never, ever deceive anyone.

I don't trust them one bit. That's why I own gold. But to act like all that gold just left our country and is somewhere else is pretty far fetched.

How is it again that inflation, fiscal irresponsibility, deficit spendig, and the debasing of our currency is a good thing? Nothing changes, the result is always the same, economic chaos. Well -DAH.

Not sure anyone is arguing that those things you listed are good. Also not sure going on a gold standard is feasible or will fix any of our ills...

taputu: IF interest rates rise several years from now, after we have regained the 8 million job losses, plus some, after California's budget is back to surplus, then both can move up together.

Right now, with millions of foreclosures still coming and a moribund job market, if rates move up it will be immediately negative for housing: every loan approval will be adjusted down in terms of maximum price by that little bit more.

"December 29, 2009, 2:05PM EST"

A lot has happened since December, most of the houses I was looking at in Dec, has shaved 30 to 40K off the price.

tapatu: So the government decided to LOWER rates... because that has no effect on home prices! So, why did the FED buy 1.5 trillion dollars in mortgage backed securities again? Because mortgage rates don't matter?

"Its not about cause and effect, but if rates go up nothing will happen to housing prices" Actually, you have managed to contradict yourself in one single sentence! Hilarious!

Rob--

When you use quotation marks, you are supposed to write verbatim what the phrase is. Not a poor paraphrase. I would think you'd have learned that at some point during your mulitple PhDs.

It's not that difficult of a concept. I'll try to explain it again for you. There is an indirect relationship between interest rates and home prices. Yes, lower interest rates are better for home prices--ALL ELSE BEING EQUAL. Unfortunately, all else is never equal. So, other factors have a larger effect on home prices than interest rates. That's all I'm saying.

other factors, such as increasing foreclosures? piss poor job market? ending credits that have encouraged buying? good points tapupu...! Housing is in real trouble!

other factors, such as increasing foreclosures? piss poor job market? ending credits that have encouraged buying? good points tapupu…! Housing is in real trouble!

Wow--you don't really want to have an objective conversation, do you? You just want to do anything you can to say housing prices will fall. OK--whatever you say Dr. Doom.

taputu: those are called factors! I would say the 100% increase in people not paying their mortgages in the past 18 months is significant, but you would prefer to dismiss it and cast insults? did you just buy a home or something that you are so desperate to cast aspersions rather than actually think?

I own some physical gold but have been thinking about selling. I have a hard time understanding why gold is so expensive. I love the US Buffalo coins however. 24 karat pure gold.

taputu: those are called factors! I would say the 100% increase in people not paying their mortgages in the past 18 months is significant, but you would prefer to dismiss it and cast insults? did you just buy a home or something that you are so desperate to cast aspersions rather than actually think?

Do you really not get it? Of course those are factors. Those are factors explaining why interest rates won't be rising (much) in the near future.

I like how you guys are pointing to Data that is over 5 months old, as solid proof the bottom was in 09.

Last I heard, last month was the worst foreclosure report on record.

I don't know what cup you guys are drinking from, but the Tea leaves are lying.

OK, I’ll ask you a question. How did the world operate when we WERE on the gold standard? Low inflation, fiscal responsibility, no currency debasing? I don’t know - thats sounds good to me.

You are perhaps somehow not aware that there was a major financial crises in America roughly every 20 years from the signing of the Declaration of Independence up to and including the great depression. Here are some hints:1797, 1819, 1837, 1857, 1873, 1893, 1901, 1907. These were just the biggies, there were smaller economic hiccups also. Widespread business collapses, stock market collapses, massive bank failures, high poverty, 20% unemployment, credit collapse, real estate collapses, high foreclosures. All of which happened on the gold standard. Sounds familiar to me. Explain again how this is utopia.

Rose colored glasses are always a good thing. Nothing changes.

Well, fractional reserve banking is an abandonment of the gold standard. It should be illegal. All these banking crises that you speak of are a symptom of paper money being substituted for gold.

I'm seriously confused. The gold standard is paper money backed by gold at a fixed rate (no one has mentioned so far that the fixed rate could be changed AT ANY TIME by a simple majority vote of congress I notice). You are arguing for going back to the gold standard. You argue that being on the gold standard will bring financial nirvana in our time. You are arguing that everything was peaches and cream before dropping the gold standard. But you are also saying that 150 years of financial crises (pre fractional lending) that happened while on the gold standard were because we used paper money backed by gold, which by definition is the gold standard. Huh? Did I miss something or did I just step through the looking glass?

You should start drinking again, bob-o. Everything is starting to make sense... :)

Personally, I wouldn't live somewhere with a requirement that I not park on the street.

Good luck enforcing a "no parking on the street" rule. Its a city street, you don't make rules for it. I lived in an HOA that had such a rule, and they got ripped apart when an owner sued over fines for parking on the street.

OK, I’ll ask you a question. How did the world operate when we WERE on the gold standard? Low inflation, fiscal responsibility, no currency debasing? I don’t know - thats sounds good to me.

You are perhaps somehow not aware that there was a major financial crises in America roughly every 20 years from the signing of the Declaration of Independence up to and including the great depression. Here are some hints:1797, 1819, 1837, 1857, 1873, 1893, 1901, 1907. These were just the biggies, there were smaller economic hiccups also. Widespread business collapses, stock market collapses, massive bank failures, high poverty, 20% unemployment, credit collapse, real estate collapses, high foreclosures. All of which happened on the gold standard. Sounds familiar to me. Explain again how this is utopia.

Rose colored glasses are always a good thing. Nothing changes.Well, fractional reserve banking is an abandonment of the gold standard. It should be illegal. All these banking crises that you speak of are a symptom of paper money being substituted for gold.

I’m seriously confused. The gold standard is paper money backed by gold at a fixed rate (no one has mentioned so far that the fixed rate could be changed AT ANY TIME by a simple majority vote of congress I notice). You are arguing for going back to the gold standard. You argue that being on the gold standard will bring financial nirvana in our time. You are arguing that everything was peaches and cream before dropping the gold standard. But you are also saying that 150 years of financial crises (pre fractional lending) that happened while on the gold standard were because we used paper money backed by gold, which by definition is the gold standard. Huh? Did I miss something or did I just step through the looking glass?

No, you are just putting words in my mouth with this "utopia" talk. You brought up banking crises of the 1800s. They are all based on the facts that banks cheated and issued more paper than gold they had in their hands. The practice of a fractional reserve system an abandonment of the gold standard. Prior to central banking in the US, this always resulted in a banking panic that restored prices to a sustainable level because they could not print their way out of a banking crisis. Ultimately, the problems caused by fractional reserve lending would get unwound through a banking crisis. This is not a problem with gold. It's a problem with fractional reserve banking. You are sorely mistaken. Fractional Reserve Lending existed during those entire 150 years of those banking crises and fractional reserve lending was ALWAYS the culprit.

I suggest you read what I actually advocated for at the beginning of this thread.

I live in a place like what Ellie calls a sh*thole.

You see, the majority of the homes on my street in East San Jose have people living places other than the house itself, like in the garages, enclosed patios on attached to the back of the homes, trailers parked in the backyards or along the sides of the house, one home with a massive RV parked along the side of the house which is a full time residence, and at least have two with shacks in the backyards with people living in them. And, among those of us who don't have such "extra" living space footprinted on our lot, almost all of us have some non-nuclear family adults living in the household who have jobs, and therefore, cars.

For the most part the "trailer/garage/shack trash" are not bad people and are not bums, it is just hard to make ends meet and hard to get by here in the Bay Area on low wage jobs.

But jeez there is a problem with parking here. People park all over the place including their front yards (needless to say, not really "lawns" anymore). I parked on my lawn sometimes, not often enough to damage it though. People used to park on the sidewalks or block them but the San Jose Parking Violation Stazi kept giving residents parking tickets so that doesn't happen much anymore. I had to clean out my garage to make parking space to deal with it.

Clearly the problem is that we backed paper with gold. If we all carried around physical gold coins and used them for all transactions we'd be way ahead of where we are today. When you buy something online, you could just shove gold coins into your monitor to pay for them.

Also, it's hard to get robbed when you carry a big bag of gold coins. You just hit the robber in the face with them.

Also, it’s hard to get robbed when you carry a big bag of gold coins. You just hit the robber in the face with them.

I actually did that once many years ago when I was working a summer job at an amusement park collecting coin from vending machines and someone tried to grab a money bag from me. Worked great.

Re: parking on the street. I have friends out in Concord, and, at least in the neighborhoods I know, there are big, generous driveways, definitely adequate for a couple of cars. It's much more spacious out there than it is in other parts of the Bay Area. In my neighborhood, there are driveways that will handle one car of modest size, so obviously it is necessary for most two-car families to have the second car parked on the street. I don't think that would be necessary in most parts of Concord. Given context, the rule makes sense.

Lets recap:

Our resident Donald Trump investor has 3 homes... count them 3.

they are 100% financed (his words)

He is "improving the neighborhood" by not allowing street parking...

He is collecting way above market rents, according to other posters who know the area...

Ok, in what neighborhood in the world is the street parking situation even going to be noticeably changed by the actions of three homes? AND, if one of the renters bought another car, how the heck would the landlord even know about it? Unless you live in one of these three homes, no way you will know who parks on the street. A dog in the house you would know if/when you came by, some car parked in the street that could belong to any of 20 homes? Nope!

This whole self aggrandizing story is BS, top to bottom. He has some homes, nothing special, no magical neighborhood improvement due to his brilliant management, no mythical super above market rents... nada.

Nothing in this passes the smell test.

defend the non-sense if it makes you feel better, be my guest!

@sf

There is a difference between parking 2 cars in the garage, or 2 cars in the driveway vs 8 cars on the street.

@zrob00

He owns his house, he can pull financing from it to use for these other homes. If he pulls 20% from his home, and 80% from the other home, how is that not 100% financed?

The rents don't sound out of line for the area. Owning 3 houses on a street would help that street out. Especially if several of the other homes are owner occupied. Assuming owners are avoiding the 8 cars per house issue, that only leaves a few more houses on a typical street. It isn't a full blown neighborhood as in 8 blocks x 8 blocks, but it could easily impact the area he is in. Especially if the street isn't very far from the main street. If you need to drive though 8 blocks of crap to find your "upgraded" street, it would be obvious. If you drive one block off the main street and you hit a decent street, people will ignore the rest of the neighborhood because they don't need to see it, or probably ever travel through it.

There are periods in history where mortgage rates went down and prices went up, correct? ~2000-2005, for example. Recently mortgage rates have dropped and prices have stabilized or have even gone up in 2009-2010. So there are points in history where your theory is not true. ~2005-2009 was kind of up in the air because of the loose lending. So instead of going back to the 1930's or 1970's, why not use recent historical data?

There are periods in history where mortgage rates went down and prices went up, correct? ~2000-2005, for example. Recently mortgage rates have dropped and prices have stabilized or have even gone up in 2009-2010. So there are points in history where your theory is not true. ~2005-2009 was kind of up in the air because of the loose lending. So instead of going back to the 1930’s or 1970’s, why not use recent historical data?

I think you're missing the point. At least what I was/am trying to say. It's certainly true that interest rates may move opposite of home prices, just as they might move in tandem with them. What the history has shown is that there really is a very low correlation between interest rates and home prices. So, despite all the posters saying once interest rates go up, home prices will fall like a rock--the data says different. Prices may go down, or they may go up. We just don't know.

« First « Previous Comments 2,278 - 2,317 of 117,730 Next » Last » Search these comments

patrick.net

An Antidote to Corporate Media

1,266,714 comments by 15,147 users - Blue, Patrick online now