Thread for orphaned comments

2005 Apr 11, 5:00pm 233,399 views 117,730 comments

by Patrick ➕follow (59) 💰tip ignore

« First « Previous Comments 4,029 - 4,068 of 117,730 Next » Last » Search these comments

You can quibble about semantics, and argue that it's only an opportunity loss. I say it's a real loss. Referring to my last comment, if you had been in cash instead of bonds, you would then be able to lock in an additional 4.25% for those 25 years. If you think of the difference in present value terms at that time, it is a huge loss.

Again, bonds and gold are saying two different things about the dollar. A good point was made about desirability of gold in Asia, maybe independent of the value of the dollar against other currencies. Seems like a lot of that value is factored in at this point.

Counting on a bubble ? Okay. I do think bonds are probably overvalued ( and may become more overvalued before a big downtrend ), and I understand the premise about gold. IT probably should be a part of everyones portfolio. Maybe that fact is enough to cause a bubble. I just don't know. I guess I can see that at some time it will happen. Maybe a decent chance it does in my life time.

I agree with Mark--bonds are saying something about global uncertainty. People want a safe place to put their money. And I agree with you that most aren't going to keep them for 30 years. Probably they will sell them at a slight discount as things improve everywhere.

The "bailout" was never intended to do anything more than payback union members for their support for Democrats. To think otherwise is just plain silly.

The taxpayer pumped some 30B to save GM and in exchange essentially got 60% ownership. Then there is a fair amount already repaid and a fair amount as preferred shares which carries an interest that the government is collecting. The union in exchange for pension relief got a bunch and the bondholder got converted to ownership as well. Existing shareholder got wiped out since they got diluted from the union, the fed and bondholders.

Structurally, GM does not have the cripping long term debt from bondholders anymore and the pension obligations are much more managable since they too are converted to shares. Instead of Pontiac, Saturn, Geo and many repeatable brand stretching their resource, the new GM will have a luxury class, a mid class and an entry class, like every other car manufacturer. So besides long term debt obligations, their business is focused on their profitable brands as well and dump the excessive brands like they should have years ago. It's not dead going forward, the demand for vechicle will be significantly above 2009 base.

Techincally, $ per share is a horrible measure of value. If there is 1,000 share outstanding, the 134 = 13,400. A more appropriate measure is total market cap and % ownership, here 50Billion market cap is 30 billion equity to the government and considered the breaking point to the extent they can sell the position at that price and above.

Ford motor company has a 43B market cap, I don't see why GM can't make more money than Ford and deserve a higher market cap given their long term debt obligations and renewed focus can put them in a position ahead of Ford.

The CEO did an excellent job to put this company back in the profitability path. I have no issues saving GM as they just need to restructure their debt (which they did converting preferred/bond holder in the commons), other long term such as pension obligations (which they did), focus on profitable brands (which they did) and rewrite some bad contracts (which they did). Now they need find a top seller. (which will be easier to accomplish now that they can invest their resource in 3 brands instead of 20)

In 20 years, you'll be glad we still have GM, Ford and Crystler.

What happened to restructuring your debt the old fashioned way, via bankruptcy court? The stockholders got the dividends all the years GM made money, not the taxpayers. Should we have saved all 548 of the car manufacturers that have gone out of business in America over the years? Would we be glad to have them?

Gm is just another example of privatized profits and socialized losses. Government should provide physical, societal, and legal infrastructure to business. That's all.

@bob

They wanted to avoid bankruptcy. Stockholders got virtually nothing in the new GM. Pensioners and the Government were about the only ones to walk away with anything.

Now the government could have just let the whole thing blow up, but the fallout would have been enormous. This wasn't just "one large company falling" it would have taken down one of the largest sectors in the US with it. We simply don't have many car manufactures now. Maybe someone would argue it would be better to have lots of small ones anyways, the problem with that is, it would be lots of small companies + ford + toyota + every major car manufacturer in the world. Those companies would kill off the small ones, leaving essentially one US based manufacturer in one of the largest sectors in the US, with everyone else being a global competitor.

Having too big to fail companies is bad, but when the other too big to fail companies aren't yours, it's a dangerous game to play. If all the major manufactures where in the US it would be one thing. New business would be created from the ashes of GM, unfortunately, the most likely outcome would be a complete loss of the automotive sector in the US.

So when do the nominations for "idiot of the year" open up? I know a Knight from Poland that I want to propose...

PolishKnight says

I could even hang out with them for a beer (especially Hillary! Scarfing down kielbalsa in PA? _I_ voted for her in the open primary!)

So you voted for the loser in a primary - just proves you were wrong about yet another thing.

PolishKnight says

I disputed it but if you want a yes or no answer, the answer is yes. Asians are considered a minority and are not considered white. Happy?

Are you asian and have an axe to grind? Heck I'm part Cherokee and my axe isn't nearly as big as yours. You need to go back to anger management class - apparently you didn't graduate "cum laude". I hope all of the tea party members aren't as mad as you.

"Two things are infinite: the universe and human stupidity; and I'm not sure about the the universe."

Take care and have a good weekend.

And don't go home and kick your dog. I'm OK with kicking cats though.

Now they need find a top seller. (which will be easier to accomplish now that they can invest their resource in 3 brands instead of 20)

In 20 years, you’ll be glad we still have GM, Ford and Crystler.

If only they actually built good cars - I bought a Chevy POS model in February and it has spent a total of one full month in the shop since I bought it. They keep saying it's fixed, then discover something else they should have done. When I mention "and another thing I noticed..." it turns out that there was a service bulletin on it - but they only fix it if you ask. I realize that it would have been bad for the economy if they'd gone under and that we have an opportunity to recoup our investment - but it would be alot better if they actually built good cars.

I wonder what the execs at Chevy really drive. Unless it's mandatory that they drive their own crappy cars, I'll bet they drive better ones. Are Hugos still around?

I don't know if they can succeed regaining market share. I really believe the sympton of their problems were too many brands. Branding is everything in the car world. It is the only reason why people buy a Mercedes over a Cadallac without regards to price.

Resource are limited and It's hard to spread investment/marketing/research dollars on too many brands, you end up with half ass efforts everywhere. BMW spends all their resource to create the best 3,5,7 series possible and put as much investment and marketing resouce it takes. I like their chances a little more now as they can just focus on one or two brands instead of 8.

Company:

Toyota, Totoya, Lexus,

DMG, Mecedes Benz

BMW BMW, MINI

Honda Honda, Acura

Nissan Nissan, Infiniti

Note how other car manufacturer's do it. Brand their products into a entry level brand and a luxory brand, that's it and it works.

Prior to the reorg, GM had a ridicoulous amount of brand, not surprisingly, they end up with no branding and Saturn, Pontiac, Geo or whatever was just the same car with different names. Now, GM focus only on Chevy, Cadillac, GMC and Buick Brand which in my opinion is still 2 brands too many. If I was the CEO, I would focus on the Chevy and Cadillac brand and discontinue the GMC and buick Brand as well. A company shouldn't be spreading their resoucre on both the Cadallac and Buick Brand, it makes no sense. At least they got rid of Pontiac, Saturn, Hummer and Geo brands

Actually Honda only has the Acura brand within North America if I remember correctly. Elsewhere it's just Honda.

I feel it's not horrendous having that many brands, however every brand they had seemed to have a bad name! I think they started to get into trouble as employees aged. The motto of "I can't be fired for what worked last year..." started to take hold. Partial fear of failure, and probably loss of creativity as people get older probably helped doom them to their current quality of cars.

Cars are not only part of our culture, but also help identify each individual. Therefore, having a whole slew of cars gives people a better chance of finding something unique among their coworkers, friends and family. I think BMW/Mercedes get away with essentially 3 models because they don't have a lot of vehicles out there. Therefore your choice is unique in a way.

"however every brand they had seemed to have a bad name!"

It's not an accident they have a bad name, A company like BMW spends all their resource on the BMW, a company like GM splits their resource into Cadillac and Buick which makes no sense to me. It's the same market segment with same target customer.

The bad name came from quality, and lack of innovation. If they had one brand, I'm betting the same team who designed it would be doing it year after year, creating the same boring cars. The same quality would come into play as well! They make enough cars that they should be able to clean up quality control. Considering how much is shared between each model, it should be pretty easy in fact! They're aiming for cheap bulk, which is going to generate a bad name regardless.

If I was blindfolded and put in a mercedes I would know I was in a mercedes, I could just tell from the quality. Close the door, quality. Get on the highway, nothing rattles, quality. These companies spend money to improve their brand and to ensure top dollar for their vehicles, but these other cars are just horrible from the bottom up!

I think there is a lot more to it than too many brands. I'm betting if honda created 15 brands, they would all sell well. Even if they were printed under another name and no one EVER knew who made them. THe quality is just there. They would all get good reputations very quickly.

Maybe you don’t understand bonds. They are long term, and there is a huge risk of loss if and when interest rates go up (and or when much inflation occurs).

Yes and no. You only lose if you try to sell on the secondary market. You’re guaranteed the stated return on the bond.

Also, not if you invest in bonds through an intermediary (like a bank or MM fund) that buys the bonds and assumes the interest rate risk, giving you a "cash balance". There is still a lot of demand for cash.

not if you invest in bonds through an intermediary (like a bank or MM fund) that buys the bonds and assumes the interest rate risk

Money market funds do not invest in bonds (AT ALL), they only invest in the shortest term securities such as 90 day treasury bills, or possibly commercial paper and other short term securities, but not bonds.

There are bond funds, but they have a very significant risk of loss of principal, just like bonds.

Maybe some people don't get this because the trend in interest rates has been down (in rates) and up in bond prices for so long.

Things keep going the way they are, and there is going to be a genuine mini wealth effect from rising PM prices in the alternative/fringe/gloom and doom investment crowd. The one thing all of these anti-orthodoxy/mainstream economic gurus have in common is a love for the yellow and silver precious. I can just imagine a mini economic boom in places like New Hampshire as a result, lol. The "nutjobs" have done far better with their investments than indoctrinated mainstreamers for several years now - I'm glad I listened to what they had to say.

How many of you bugs on this thread follow Max Keiser, Gerald Celente, VisionVictory (Daniel on his Youtube channel), Marc Faber, Peter Schiff, Jim Willie, etc.?

Anybody have any additional "nutjobs" that would be good recommendations for me? Thanks in advance.

Things keep going the way they are, and there is going to be a genuine mini wealth effect from rising PM prices in the alternative/fringe/gloom and doom investment crowd. The one thing all of these anti-orthodoxy/mainstream economic gurus have in common is a love for the yellow and silver precious. I can just imagine a mini economic boom in places like New Hampshire as a result, lol. The “nutjobs†have done far better with their investments than indoctrinated mainstreamers for several years now - I’m glad I listened to what they had to say.

How many of you bugs on this thread follow Max Keiser, Gerald Celente, VisionVictory (Daniel on his Youtube channel), Marc Faber, Peter Schiff, Jim Willie, etc.?

Anybody have any additional “nutjobs†that would be good recommendations for me? Thanks in advance.

Keiser and Celente are entertainers. Marc Faber is no nut job. Marc Faber is probably the greatest economist living today. Schiff is pretty smart but a lot of his arguments are rhetoric rather than describing the actual process. That being said, I owe Peter a big one since he recommended to me to pick up Skyworth Digital 2 years back.

Maybe you don’t understand bonds. They are long term, and there is a huge risk of loss if and when interest rates go up (and or when much inflation occurs).

Yes and no. You only lose if you try to sell on the secondary market. You’re guaranteed the stated return on the bond.

With the interest rates being doled out by the bond market now, you are pretty much guaranteed a return damn close to 0.1% annually. When inflation comes alive, those returns become -1% or -5% annually in real terms. Buying a long term bond earning under 6% with the plan of holding it to maturity is suicide today. People piling into the bond market are nothing but your modern day condo flippers looking to unload their garbage on the foolish masses. In 4 years time, we'll have all kinds of experts on TV trying to explain why no one understood that a 10 year bond that earns 1% with no risk of default is not a good or safe investment.

Money market funds do not invest in bonds (AT ALL), they only invest in the shortest term securities such as 90 day treasury bills, or possibly commercial paper and other short term securities, but not bonds.

Money markets in fact do invest in long term debt, just not directly. You have to follow the chain to the ultimate debtor.

Just take a look at VMMXX. #2, #3, #4 holdings are short term mortgage securities. OK, short term.....but what are those securities backed by? Long term mortgage debt. The GSE is just another intermediary. Your "money market" cash is backed by a short term GSE security, which is backed by a 30 year mortgage.

Much of the rest is finance companies like GE, Toyota, and banks. What are their holdings in? Multi-year debt.

Money market funds provide a huge demand to the the bond market.

Money markets in fact do invest in long term debt, just not directly

When there is only six months left on a 20 or 30 year bond, then it is a short term security, that could be part of a money market fund. That is the one and only sense in which you are correct.

http://en.wikipedia.org/wiki/Money_market

http://en.wikipedia.org/wiki/Money_market_fund

Money market funds provide a huge demand to the the bond market

You're a smart guy, so sometimes when you make something up, it's going to be correct. But not in this case.

Your VMMX:

Characteristics as of 08/31/2010

Number of holdings 303

Average maturity 58.0 days

Weighted average life 116.0 days

Fund total net assets $107.8 billion

Portfolio composition

Distribution by issuer (% of fund) as of 08/31/2010

Prime Money Mkt Fund

Bankers Acceptances 0.0%

Certificates of Deposit 17.2%

Commercial Paper 17.7%

Other 0.0%

Repurchase Agreements 5.3%

U.S. Govt. Obligations 23.4%

U.S. Treasury Bills 16.8%

Yankee/Foreign 19.7%

Total 100.0%

I don't see the mortgages here, but a short term mortgages, say a mortgage with 9 months left on it is not really related (in price) to mortgages with over 20 years till maturity. And buyers of such short term mortgage securities are not putting a dent in the supply of long term mortgage securities that need to be sold. The backing has to do with how secure they are, not the price (the interest rate). Assuming low risk, the price is determined by comparison to other securities of similar risk and duration.

I don’t see the mortgages here

I think you're missing my point. No, I'm not saying money market funds own mortgages, but they do buy short term securities, which ultimately go to fund mortgages. I'm not making anything up.

https://personal.vanguard.com/pdf/hold0030.pdf?cbdForceDomain=false

#2 "Federal Home Loan Mortgage Corporation" $11 Billion

Freddie Mac, borrows funds short term, and lends them long term, much like any other other financial entity. Holders of VMMXX, a money market fund, are providing funds ultimately to long term mortgages. The money market fund is not buying mortgages that have 9 months left, it's buying short term notes issued by Freddie Mac (about 1/3 of Freddie Mac's debt is short term), and Freddie Mac is turning around and lending long term to homeowners.

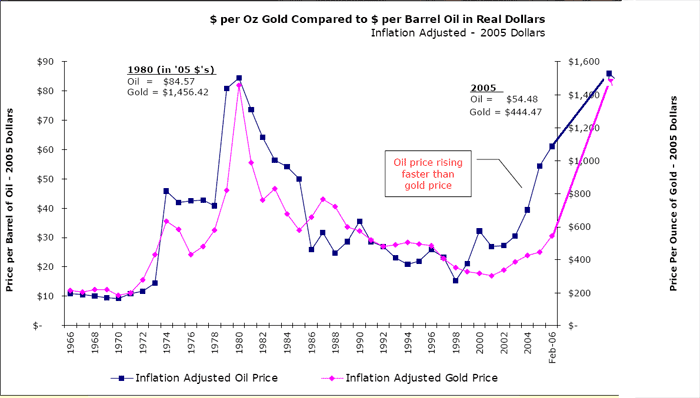

More importantly there is also the commodity aspect, which is fairly independent of USD deflationary forces.

Just to elaborate this point, here is a comparison of gold and oil prices (I took the liberty of modifiying the chart to reflect present prices. Chart was from 2006, and noted that oil was rising faster than gold. Since them they are right about the same again)

Note that the chart is inflation adjusted so the spikes have nothing to do with inflation.

Gold price is mostly just a function of increased demand from BRIC countries for commodities. China now buys more oil from Saudi Arabia than the US.

It has not much to do with anticipating inflation, sovereign default, etc.

Mark,

Cool graph.

Inflation is a monetary thingee, not exactly the same thing as "rising prices" though it can (and often does) lead to higher prices. But not necessarily so.

We can have deflation and rising prices and I think it is happening.

it’s buying short term notes issued by Freddie Mac (about 1/3 of Freddie Mac’s debt is short term), and Freddie Mac is turning around and lending long term to homeowners

Okay. That's interesting. Freddie Mac ends up with a huge yield curve position, which they could hedge in the regulated derivatives markets (exchange traded financial futures and or options). So you were right after all about demand to long term securities (sort of, because the hedge undoes some of that- but let's not go there).

But weren't we talking about investors in Money Markets Funds ? All they are really getting, in terms of risk reward is an investment in short term securities. They are not taking on any of the price risk associated with investing in long term bonds. Which at least from my perspective was what we were talking about.

I say nonsense

And I would still say that gold is saying something. IT turns out that strength in the economy usually goes hand in hand with increased inflationary expectations. That is the reason why gold often goes up in tandem with industrial commodities.

Gold is bought in prosperous times as gifts and in jewelry and so on. But it is also a substitute for money. One that does not have monetary inflation risk.

So certainly part of gold's appeal is as an inflationary hedge, and more singularly as a possible BIG winner in the event of some sort of dollar crash, or inflationary crisis.

And I still say, my opinion is that gold and bonds are contradicting each other. Maybe that has to do with government involvement in the bond and mortgage markets. Or maybe it has to do with hedging, or people paying a premium for perceived safety. But if and when gold gets bubblishious (sp?), there will be inflationary inferences associated with that phenomenon.

The last really big precious metal bubble(1980) peaked at a time of unprecedented inflationary expectations, along with the manipulation of the Hunt brothers.

So….If you think people are buying gold as inflation hedge, where are the people buying RE as an inflation hedge?

I have been talking about gold price increases being contradictory to what is happening in bonds. Okay, yes, it's also contradictory to what is happening in real estate. And yes there is leverage with real estate, as well as other aspects to the debt/credit component.

I don't claim to understand why gold is as high as it is. In fact, I see it as at least 50% chance that it will be lower in price one year from now.

Real estate is a MUCH better deal if you expect inflation

Real Estate, tied at least in part to wages, and to its utility, does well from actual long term inflation, although eventually I guess everyone starts to believe it only goes up. That shouldn't happen again for a while.

Gold on the other hand, can have a relatively rapid price spike based on expectations alone. That is, expectations of currency devaluation or inflation, or possibly other global crises.

Thanks rentalinvestor, I did try adwords for several years, but it never made much, anywhere from $300 to $900 per month.

Only one in 2,000 readers would click on an ad. I could be more pushy about placement, but I don't like doing that.

Adwords rates have been increasing since about 2008. So those rates could have increased; however, Adwords is best for generic sites and sites with few visitors. No overhead sales costs, all managed by google, and it brings in a little site cash to those sites, who would otherwise have no way to earn any income.

Something like Patrick.net requires selling fairly directed products. Targeted affiliate programs would be much more profitable. Letting google try and match up ads with the site is pretty weak. The rates are low, and match rate probably horrible (eg Realtors, or gold coin sellers). However, using affiliate programs, he could target bank financial services to viewers. His user base is coming here because they're looking for information on housing. If they're not buying a house, it likely means they're open to other financial services. Based on his user statistics available through quantcast, he has a fairly educated and highly paid user base. These users would best benefit from educated services, worth their time, not get rich quick schemes and sham gold sellers.

I'm back!

I don't have anything to say to Eightball that hasn't already been said above. That's all. Take care everyone.

"The latest changes in the Case-Shiller national index represent a three-month moving average -- for May, June and July. Sales in May and June were inflated by government tax credits that have since expired."

Here is what Calculated had to say today:

Case-Shiller Headlines

The headlines on Case-Shiller seemed contradictory this morning. Here are a few examples:

From the Financial Times: US home prices slip in July

From the WSJ: Home Prices Rose in July

From CNBC: US Home Prices Slipped In July And May Stabilize Near Lows

From MarketWatch: Home price growth slows in July

From HousingWire: S&P/Case-Shiller 20-city composite index rose 0.6% for July

The reason for the confusion is S&P Case-Shiller reports both seasonally adjusted (SA), and not seasonally adjusted (NSA) data. Because of concerns about the impact of foreclosures and government programs on prices, S&P switched to reporting NSA numbers in their press release, but many analysts are still using the SA numbers (I reported the SA numbers - see this post for the SA graphs from earlier this morning).

The important points are:

1) this is a three month average of May, June, and July. Seasonally this is the strongest time of the year for house prices.

2) sales collapsed in July, so the next report (for June, July and August) will probably show falling prices.

Date of sale in this context means date of closing the sale, not date of contract.

Case-Shiller is based on date of CLOSING the sale, which means that tax-credit transactions are distorting the market several months after the credit officially expired.

The tax credit is based on date of contract agreement, with some leniency as to when the sale closes.

What mthom said.

The delay between contract and closing, plus the 3-month moving average means that C-S will stay up until September's numbers are released on Oct 28, although sales already tanked in July.

This is Calculated Risk's prediction, and I think he is correct.

I'm betting we're more 1994 than 1995. A July decline would have been catastrophic -- an August decline less so... but still not good.

Easy mthom - this thread may make the Patrick.net book of world records.

This may be the first time that the Case-Shiller index was discussed without any name calling, or lashing out !!!!

This is a pleasant debate : )

SF 11.2% increase. Whew! Can someone back this up by some numbers coming from the field?

It's worth noting that the top tier ($621,684) in the SF Bay Area index continued to drop (again) this month from 149.1 to 148.5. It peaked in May at 150.07.

« First « Previous Comments 4,029 - 4,068 of 117,730 Next » Last » Search these comments

patrick.net

An Antidote to Corporate Media

1,266,905 comments by 15,148 users - beershrine online now