Thread for orphaned comments

2005 Apr 11, 5:00pm 197,293 views 117,730 comments

by Patrick ➕follow (61) 💰tip ignore

« First « Previous Comments 2,751 - 2,790 of 117,730 Next » Last » Search these comments

Here is your answer E-man :

http://www.centralvalleybusinesstimes.com/stories/001/?ID=15473&source=patrick.net

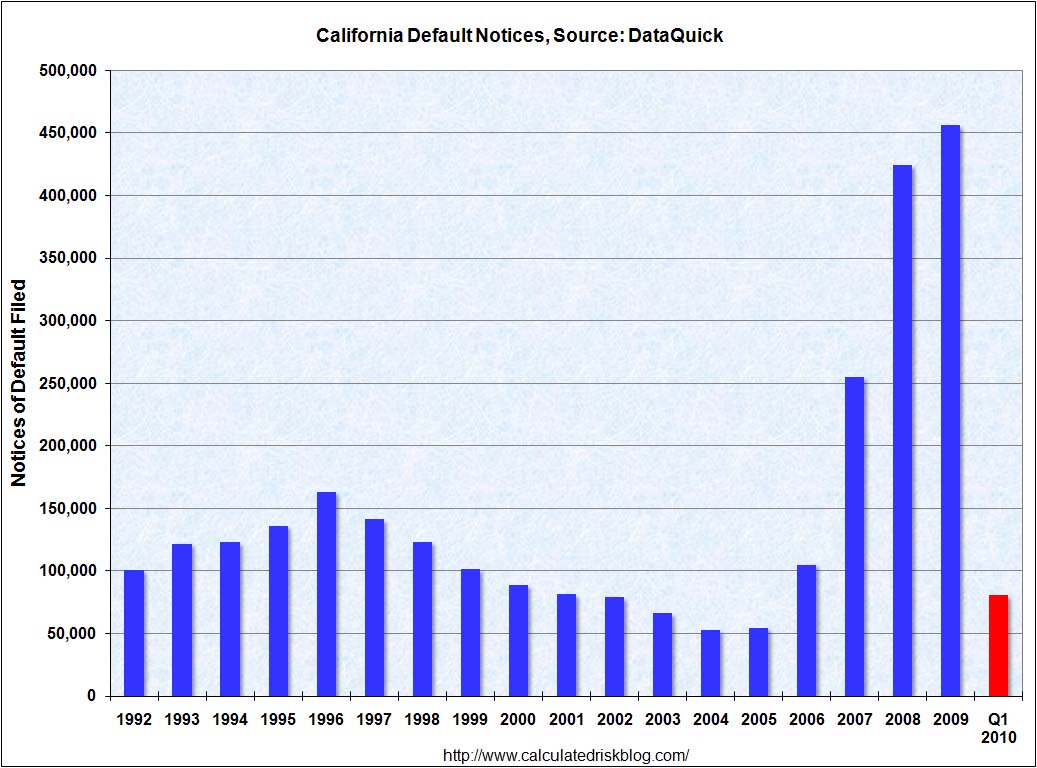

"Foreclosure activity of all kinds dropped across most of California last month, perplexing the experts.

Given the percentage of delinquent home loans in California, “this drop in activity makes no sense,†says Sean O’Toole, president of ForeclosureRadar Inc., of Discovery Bay, a company that tracks the state’s foreclosure activity on a daily basis.

“I would love to say it was due to short sales or loan modifications, but I see little evidence from residential home sales, or HAMP reports to support that theory,†says Mr. O’Toole.

Increasingly it seems that the banks and the regulators that in the past have forced the liquidation of non-performing assets, “are simply waiting and wishing for a return to peak prices reached during the bubble,†says Mr. O’Toole."

Still trying to beat a dead horse huh. This is not what the people on this board want to hear. Your comments should have been NOD up 43.3%. NTS up 35.8% and foreclosure is way up 141.3%.

Now that sounds a lot better :o)

From the perspective of someone living in NJ, that California real estate looks dirt cheap. If I want to buy a piece of crap 2 bedroom cape house with a rotting roof, tiny bedrooms, a tiny kitchen, a tiny bathroom, all of which, have not been updated since the early 60s, it's going to cost me 250k minimum, 350 to 400k in certain towns.

I'm not sure what a cape house is, but other than that, your description fits this one well, except for the price:

http://www.redfin.com/CA/Los-Altos/26-Pasa-Robles-Ave-94022/home/632537

Extend. Pretend.

I'm not really sure which bearish prediction you're referring too. Homes entering the foreclosure pipeline had to peak some time. That doesn't mean it's peaked in every region, esp. the ones slow to get started, and it doesn't mean prices are about to go up in any sustainable way.

My Ivy Zelman "classic" chart (that I have been carrying around in my wallet for the past three years) says, "Hang on, more fun around the corner".

with only 6 months past in 2010, we get this story: http://www.mercedsunstar.com/2010/06/16/1461382/property-values-in-merced-county.html#storylink=omni_popular

RE is local .... keep your eye on the ball folks.

I would guess he's referring to the ARM reset chart posted back in 2007. By that chart bottom in 2012. It's funny how if you said that in 2007 people thought you were a perma-bear nutjob.

I haven't seen that updated in a while. I kind of wonder with all the special programs and extend & pretend how it looks now too.

No need to foreclose when you can't sell the asset. You have to measure everything with incentives. The banks have a cost to foreclose like $15K or more in legal fees I think. Why do it when you'll just be stuck with the falling asset. Better to leave it in the name of the delinquent and let him/her pay the taxes and maintenance. Bankers aren't stupid. That's why they manage your money.

Its already being covered in another thread: http://patrick.net/?p=403806

I was told more houses are coming onto market in, say, Orinda and prices are getting marginally better than a year ago (e.g. from 800K to 700K). Houses stay on the market for a long time in Lafayette which probably means people expect better prices in the future. But strangely enough in quite comparable Danville houses are sold almost within a week, at least those without HOA.

Now is what it is. Comparing now to YOY is deceiving since a year ago things were total shit.

Comparing 1 year from now to now is the interesting question.

Mortgage rates higher or lower? Will FHA, FRE, and FNM even be around???

Will there be a tiers 5, 6, 7 for the long-term unemployed or will they just be f---ed?

State and local government -- spending more or spending less?

Federal government --- doing better or fallen to the Teabag Insurrection taking their government back?

Peak reset and recast is next year, btw.

{kind=link}

Now is what it is. Comparing now to YOY is deceiving since a year ago things were total shit.

Comparing 1 year from now to now is the interesting question.

Mortgage rates higher or lower? Will FHA, FRE, and FNM even be around???

Will there be a tiers 5, 6, 7 for the long-term unemployed or will they just be f—ed?

State and local government — spending more or spending less?

Federal government — doing better or fallen to the Teabag Insurrection taking their government back?

Peak reset and recast is next year, btw.

Thanks for posting the chart. This is the latest info I've seen

It should be a law that people who say inflation should have to specify which they're talking about.

Monetary inflation? Producer price inflation? Wage inflation?

Senate couldn't get the UI extender passed this week, already. 4.8 million people are on tiers 1 through 4.

'conomy isn't going to be able to absorb these people this year, no way. 900,000 already abruptly to be soon pushed off the dole thanks to the continuing Senate fail, with another similar batch arriving every month. Gulf coast becoming a toxic mess at the start of the summer vacation season's not going to help employment, though I guess domestic tourism is something of a zero-sum so that will net out elsewhere.

As I argue here every day, it wouldn't surprise me to see gas go to $10/gallon. Milk at $5. I just fail to see how this price inflation is going to push up wages. In theory and past history, wage earners in pain go to the boss with ultimatums and get raises. That going to happen this decade???

http://research.stlouisfed.org/fred2/series/UNRATE

says otherwise, and that's WITH ZIRP

http://research.stlouisfed.org/fred2/series/FEDFUNDS

and high social spending

http://research.stlouisfed.org/fred2/series/A063RC1

and high overall spending

http://research.stlouisfed.org/fred2/series/AFEXPND

we're about where we were economically in 1982, but that was a Volcker recession, not the balance sheet recession we're in now.

Back then we had a better trade balance:

http://research.stlouisfed.org/fred2/series/BOPBCA?cid=125

and gov't spending as percent of GDP was 30% less, and gov't DEBT as percent of GDP was at a post-Depression low of ~30%, compared to 100% now.

I fail to see how anyone can be bullish on the present economy. The political system is beyond dysfunctional, FFS a Christian Dominionist /Tea Party twit is outpolling the majority leader in this election cycle.

Democratic control of the Senate is in doubt. Wouldn't surprise me if they lose it.

I see catastrophe down the road. Well, not right now, I'm now off to Yosemite to catch the sunrise. see yah!

E-man:

As those slides imply Extend & Pretend is not a long term "solution". You should also note that they've been trying Extend & Pretend for almost 2 years at least now.

How much longer do you think they can keep it up? 2 more years? 5 years? A decade? You know Japan tried the same thing and things still haven't recovered after over 20 years right?

Personally I think they've about reached the end of their rope as prices are declining in general once again despite absolutely incredible market support via the GSE's, rule bending, and straight up bail outs. Oh they can continue to slow the losses with more mortgage moratoriums (I personally don't see a bottom until 2015 or 2016), but stopping them is out of the question on either the high, mid, or low range homes.

It doesn't matter what the government tries to do, people can only afford to pay only so much given their wages. Wages are still declining while things are getting more expensive, while services are being cut, and while they're being taxed more. On top of that people in general are _overloaded_ with debt.

Did you know that DTI's of 40% are common these days on so called "prime" loans? This alone guarantees that we'll be seeing higher than normal levels of defaults for years to come.

You gotta be crazy if you think we've seen a bottom in an economic environment like that. We're looking at our own version of the Lost Decade, a low key but looong term Depression is the best we can hope for at this point.

... "denial" ....... "floats your boat" ..... lmao, where is Mikey on this one?!

It should be a law that people who say inflation should have to specify which they’re talking about.

Monetary inflation? Producer price inflation? Wage inflation?

Senate couldn’t get the UI extender passed this week, already. 4.8 million people are on tiers 1 through 4.

Sorry Troy, Buth these same people havent a clue regarding push-pull inflation.

The Truth is out now. The FED colluded with the banks to keep inventory off the market, while they goosed up the bank reserves. Any talk of any kind of a recovery in the house market, is just plain silly, and equivalent to a boxer who has just been KO's, still waving his gloves in the air:

http://truthiscontagious.com/2010/06/16/the-next-housing-crisis-2?source=patrick.net

I personally think it's already a bottom for real estate as well. Prices will always be a mortgage with the same payments (excluding property taxes) as renting, with a 20% down payment or so.

In other words, I agree that low interest rates will cause higher home prices. The only thing that prospective buyers would need to worry about are rent prices.

Cash buyers (or flippers I should say) need to be careful that they are not in the process of flipping when interest rates rise.

They also need to be aware that their potential buyers are all the prospects that they have beat out with their cash offers (or not) on that property. You can be sure as hell that once the properties get relisted after renovation, that there will be negative comments from both buyers and buyer agents.

Interest rates will not rise. Kondratieff winter clearly states:

Rates fall, then they rise again, then they fall much lower:

The FED can no longer lower rates, they ran out of ammunition to prevent K-Winter. But they cannot raise them either.

> Do you realize that people invested in bonds VERY NEARLY lost every penny they had in 2008?

You must be talking about MBS bonds, not the T-bills. People who had T-bills (those are the savers that I am talking about), actually made money. The MBS bond holders should have lost every penny they invested. Instead the FED transferred their losses to the tax-payers, in fact just delaying the inevitable dooms day. You speculators got a great present from the FED in 2009, you got one last chance to get out, lick your wounds, and start all over. But, since you are a greedy SOB that you are, you will not take this chance. You learned nothing in this crash of '08, and you will be paying the piper for a long time to come.

Corporations and municipalities are speculators too. In fact most of municipalities were themselves investing in MBS's. All of these bond holders should have lost all their money, but, instead the FED saved them, at the expense of the tax payers, and the responsible people. Everybody was drinking from this RE punch bowl, except the savers, and the renters. But, when the entire sovereigns start to drop out like flies, they won't be anybody to save them.

The kondratieff wheel clearly shows you that the inflation cycle is 1/2 of the k-cycle. 70/2 = 35.

But, amazingly that didn't happen. Precisely because the k-winter must continue.

Again, like I said, forget the $USD. The $USD itself is a manipulated commodity. Oil prices, stock markets are all subject to FED manipulation. But manipulation can not last long. Eventually all prices fall back to what they should be, according to the k-cycle.

The fact that you can still borrow $1 million is, again, a sign that the BOTTOM is nowhere in sight.

Nomograph - I am afraid that it is you who is full of nonsense. FED is buying T-bills & stocks (ever heard of the plunge protection team - that's synonymous with the FED). The banks are buying T-bills because they are playing the carry-trade game with FED's money.

Factual information actually runs right along with my hypothesis. Sales are down 35% ever since FED stopped propping up the housing market. Case-Shiller is already showing prices falling:

> Even Case-Shiller admits that the winter quarter decline is seasonal. T

That I didn't hear. I did hear them admitting, however, that their season-adjusted formula is broken because we had a declining market for the last 3 years.

Also, a 35% reduction in sales is nothing to scoff at. This is a huge blow to the housing market, and will, just like it did in 2007, result in a huge price declines down the road.

Nomo has waxed eloquent. He's not blowing smoke, peeps. Yeah, he's a keeper all right. I knew he could wing it.

But I do wonder why San Diego didn't call out the SWAT team?

Like a ship without an anchor

Like a slave without a chain

Just the thought of that RE market without credit

Sends a shiver through my veins

Yes, but prior to the last decade, Argentina has had a housing collapse which makes Las Vegas look like a child's play.

When Bay Area prices drop like Argentina in the 80's, whoever is left to pick up the rubble, will be paying cash too.

Those countries which never had any credit, never enjoyed any house bubbles like the US did. As soon as any country introduced credit, house prices took off.

I wore my yellow jacket to the Hornets game in the New Orleans metropropolis area, but I stick out as a WASP.

You spelled it all correctly, c-o-r-r-e-c-t-l-y, correctly.

Aka the top 1% who actually have enough money to matter!

I keep reading time and time again how this so called 1% keeps going broke. Sports athletes, hollywood movie stars and now some locals. Today is another example you may have read about. Just how do you burn $200M in under 10 years ? Ever pay for a $6M pussy cat.. seems this guy did.

On the Eve of an IPO, Tesla Founder Elon Musk Claims He's Broke

Musk, who co-founded PayPal and cashed out for $200 million, says he invested his last $35 million in Tesla Motors -- just as the company prepares to go public.

As part of his divorce proceedings, Musk reported he had just $8,255 in monthly income and $650,000 in liquid assets, with $200,000 per month in expenses.

Elon Musk, eh?

Now there sounds like a real fine upstanding nose to the grindstone EdwardsDeming kinda American Gothic work ethic that a conservative Japanese company like Toyota would really like to partner with, ya think?

« First « Previous Comments 2,751 - 2,790 of 117,730 Next » Last » Search these comments

patrick.net

An Antidote to Corporate Media

1,250,102 comments by 14,908 users - FuckTheMainstreamMedia, justme, Kepi, Misc, Patrick, stereotomy, Tenpoundbass online now